The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance. If you would like to speak with the team call us +44 0330 341 1000, email contactbcis@bcis.co.uk or fill in our demonstration form

Published: 31/03/2026

Against a backdrop of geopolitical tensions and persistent cost pressures, BCIS chief economist Dr David Crosthwaite examines how UK construction materials and products suppliers are positioned to withstand further volatility, and what this means for long-term supply chain resilience.

Are UK construction materials suppliers positioned to weather further volatility?

Recent geopolitical tensions have brought renewed attention to the pressures facing domestic construction materials and product suppliers.

Energy price volatility threatens to squeeze manufacturers at a time when construction demand remains subdued and there’s a risk that prolonged unrest could undermine supply chain resilience in the long term.

While the latest data do not yet reflect current instability, they point to a weakening underlying position over the past decade. Lower material volumes and softer demand across key sectors suggest parts of the supply chain may be entering this period from a position of reduced resilience.

In 2025, 41 million tonnes of sand and gravel were sold in Great Britain, 22.3% lower than the volume in 2015, according to Department for Business and Trade (DBT) data(1).

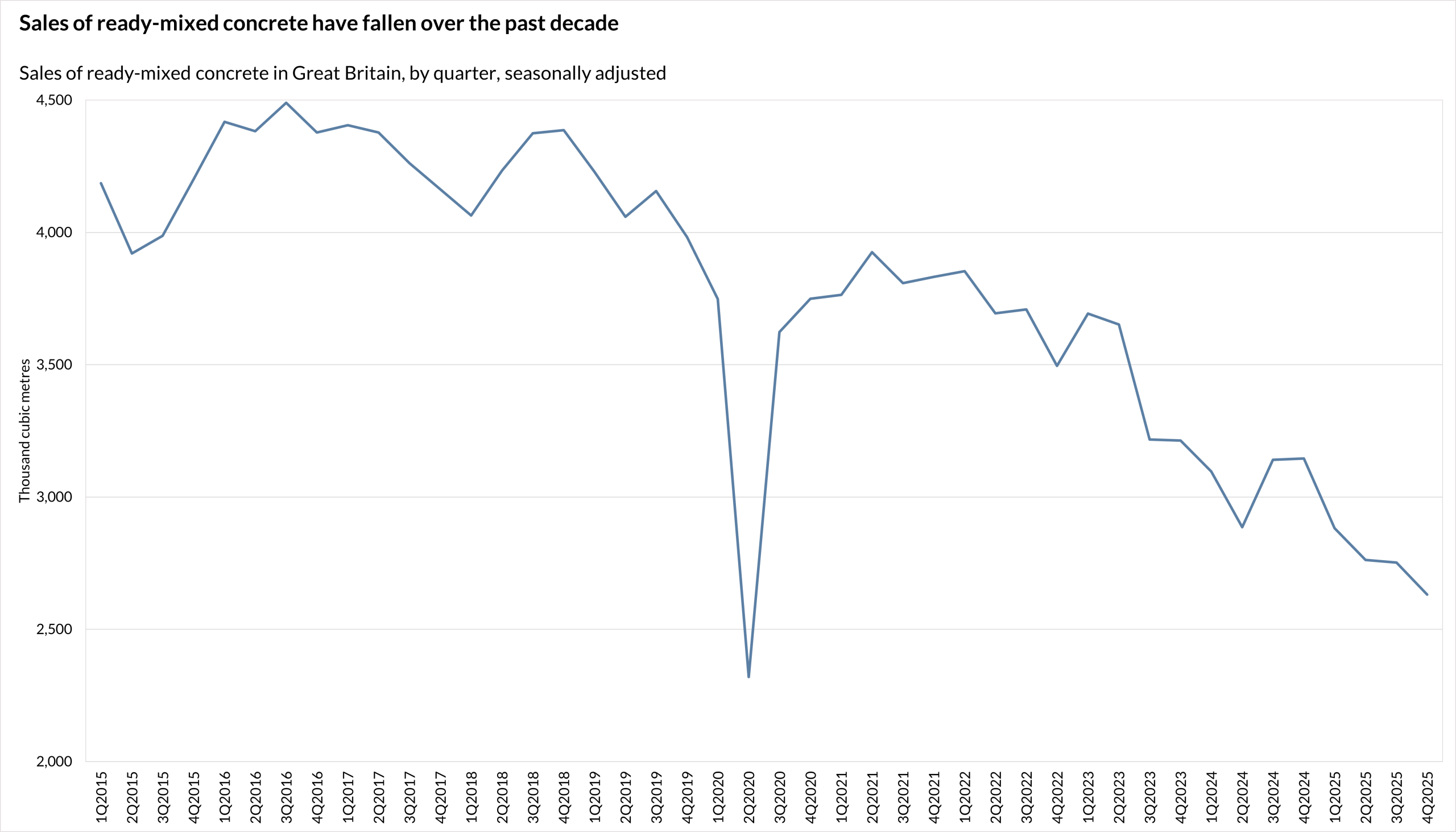

Ready-mixed concrete deliveries show a similar pattern. Volumes fell by 32.3% between 2015 and 2025, with 4Q2025 recording the lowest quarterly level on record, excluding 2Q2020.

Source: Department for Business and Trade – Construction building materials: tables February 2026, Table 6b

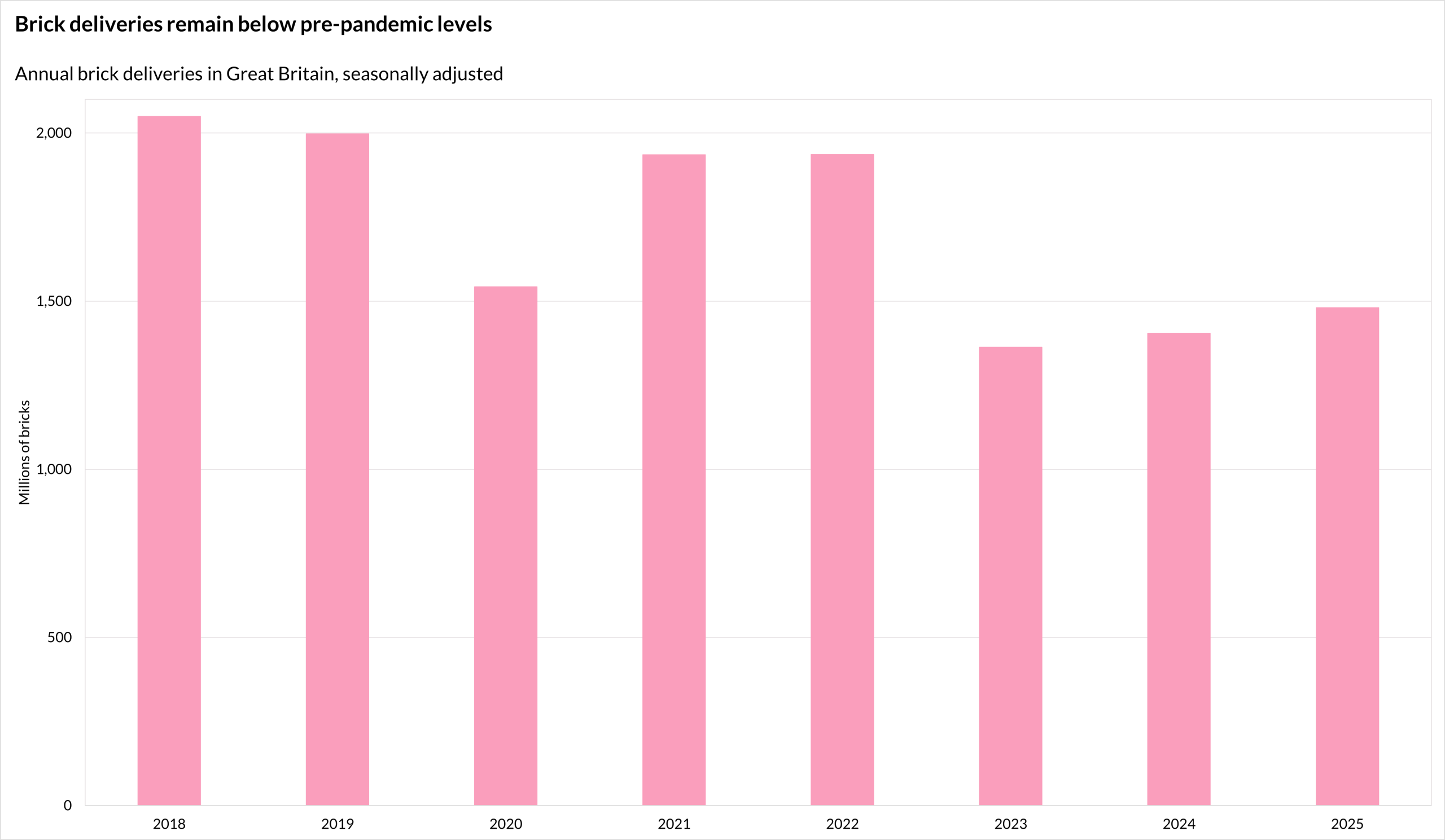

Brick data provide further insight into demand conditions. Deliveries have declined in recent years, despite a modest 5.4% increase in 2025 compared with 2024. For example, last year’s deliveries were 25.9% lower than lower than pre-pandemic 2019 deliveries.

Source: Department for Business and Trade – Building materials and components statistics, Table 9c

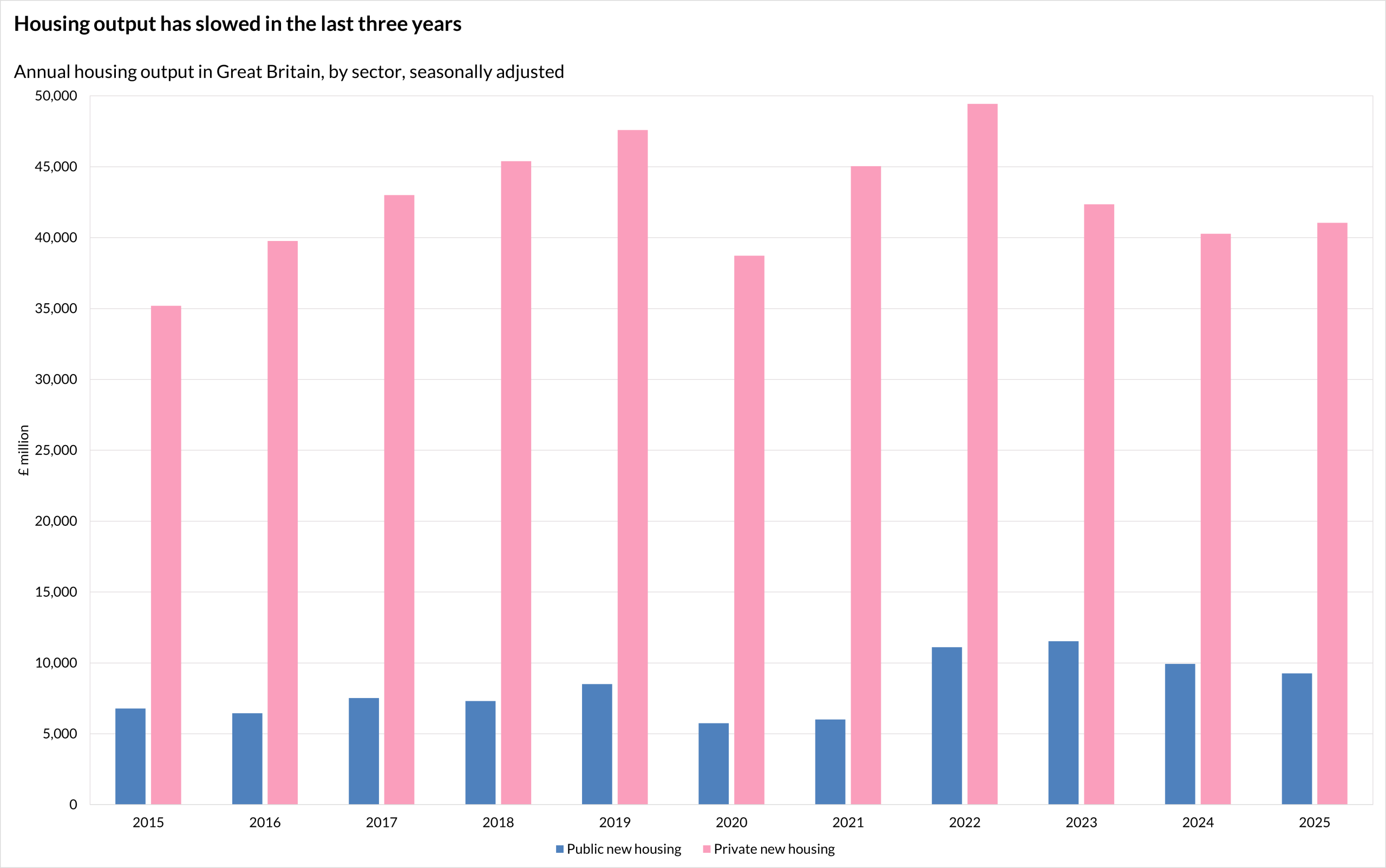

At the same time, brick stocks have increased, with notable rises in 2023 and again in 2025. This is consistent with weaker new housing output. Annual new housing output recovered after the pandemic but fell year-on-year between 2022 and 2024, stabilising in 2025 (2).

Source: ONS – Output in the construction industry, Table 2a

Taken together, the data suggest manufacturers have adjusted production in response to a slowdown in residential construction. This is also apparent in trading updates from materials suppliers, which cited subdued housebuilding as a driver of weaker performance in the second half of 2025.

Demand weakness is not confined to the residential sector. Of the last eight years, 2025 saw the lowest annual level of concrete block deliveries. Total stocks stood at 8.7 million square metres by the end of the year – 32.2% higher than the volume at the end of 2024 and nearly two-thirds above the annual average between 2020 and 2022.

Industry data reflect the same trend. The Mineral Products Association (MPA) reports that demand for concrete, aggregates and asphalt fell for the fourth consecutive year in 2025, with annual sales volumes at historically low levels(3).

According to MPA, weaker demand and rising costs have led some suppliers to reduce capacity, defer investment and mothball sites – decisions that may limit both suppliers and the wider construction sector’s ability to respond if demand recovers.

These conditions reflect ongoing constraints on housing and infrastructure delivery. Some pressures are beginning to ease, including faster decision-making by the Building Safety Regulator and stronger investment signals from the updated Infrastructure Pipeline from NISTA.

However, these are recent developments and do not offset the cumulative impact of earlier shocks, including the pandemic and the energy market disruption following Russia’s invasion of Ukraine.

Construction activity is sensitive to both investment cycles and input cost pressures, increasing its exposure to wider economic shocks. Recent conflict in the Middle East introduces a further source of uncertainty before the effects of previous economic shocks have fully worked through the system.

For construction professionals, this has implications for both pricing and the availability of materials, particularly where reduced capacity limits the sector’s ability to respond to any recovery in demand.

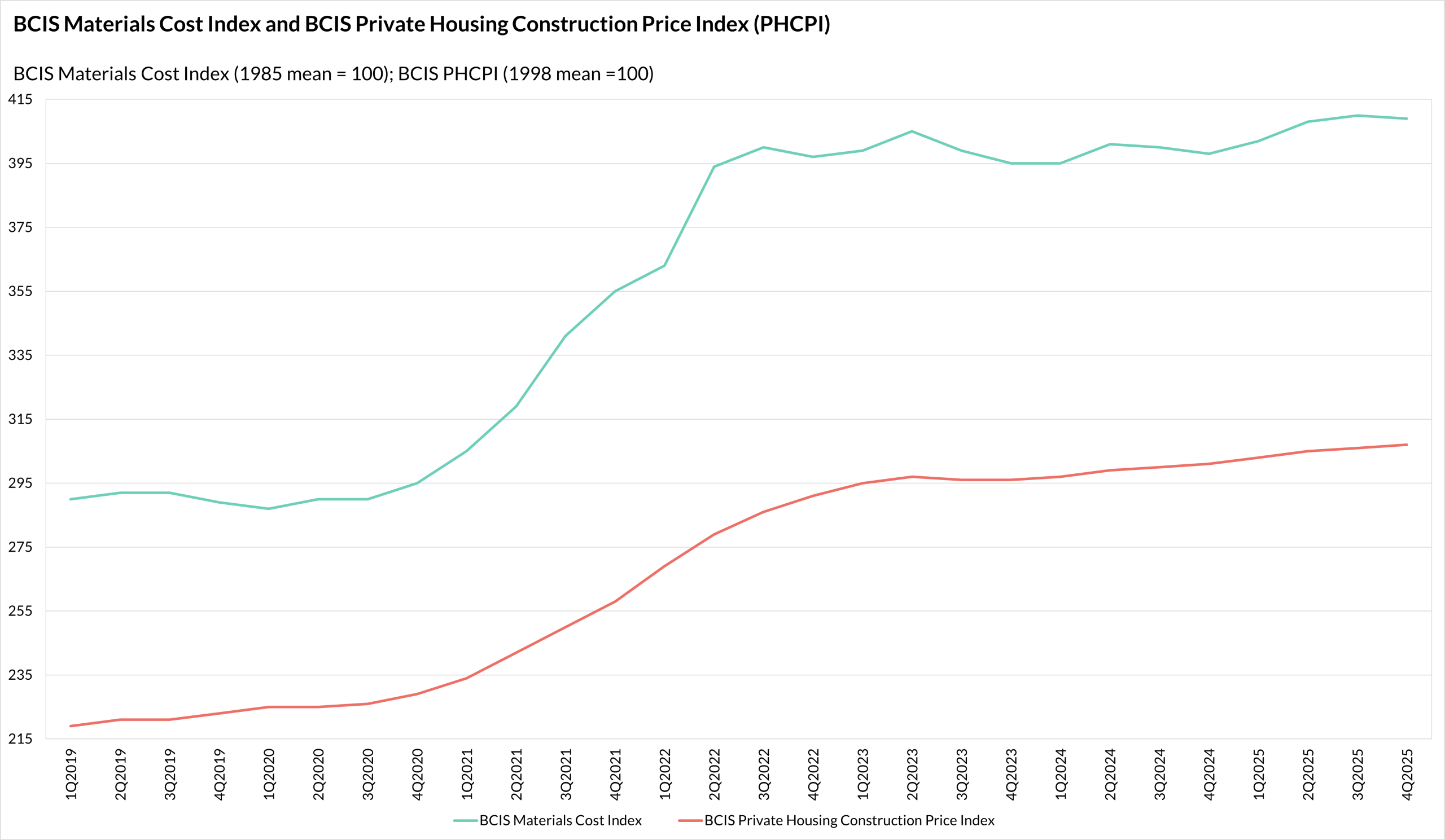

For example, materials costs remain elevated above the trajectory seen before Russia’s invasion of Ukraine in 2022. This is reflected in construction prices. The BCIS Private Housing Construction Price Index, which measures prices paid by housebuilders, increased by 8% between 1Q2022 and 4Q2022, and has maintained a higher price level since.

Source: BCIS

At present, the outlook for domestic suppliers remains uncertain. Nearly six weeks into the conflict, it’s likely energy price volatility will now compound existing cost pressures and feed through into higher pricing for construction materials and products. This could further suppress demand and reinforce the cycle of weakness.

Recent government commentary(4) indicates that energy prices remain materially higher than pre-global energy crisis levels, despite falling from the peaks seen between 2021 and 2023.

Policy measures such as the British Industrial Competitiveness Scheme aim to reduce electricity costs for some energy-intensive industries from 2027 but this does not address near-term cost and demand pressures and, subsequently, the greater risk of insolvency for suppliers.

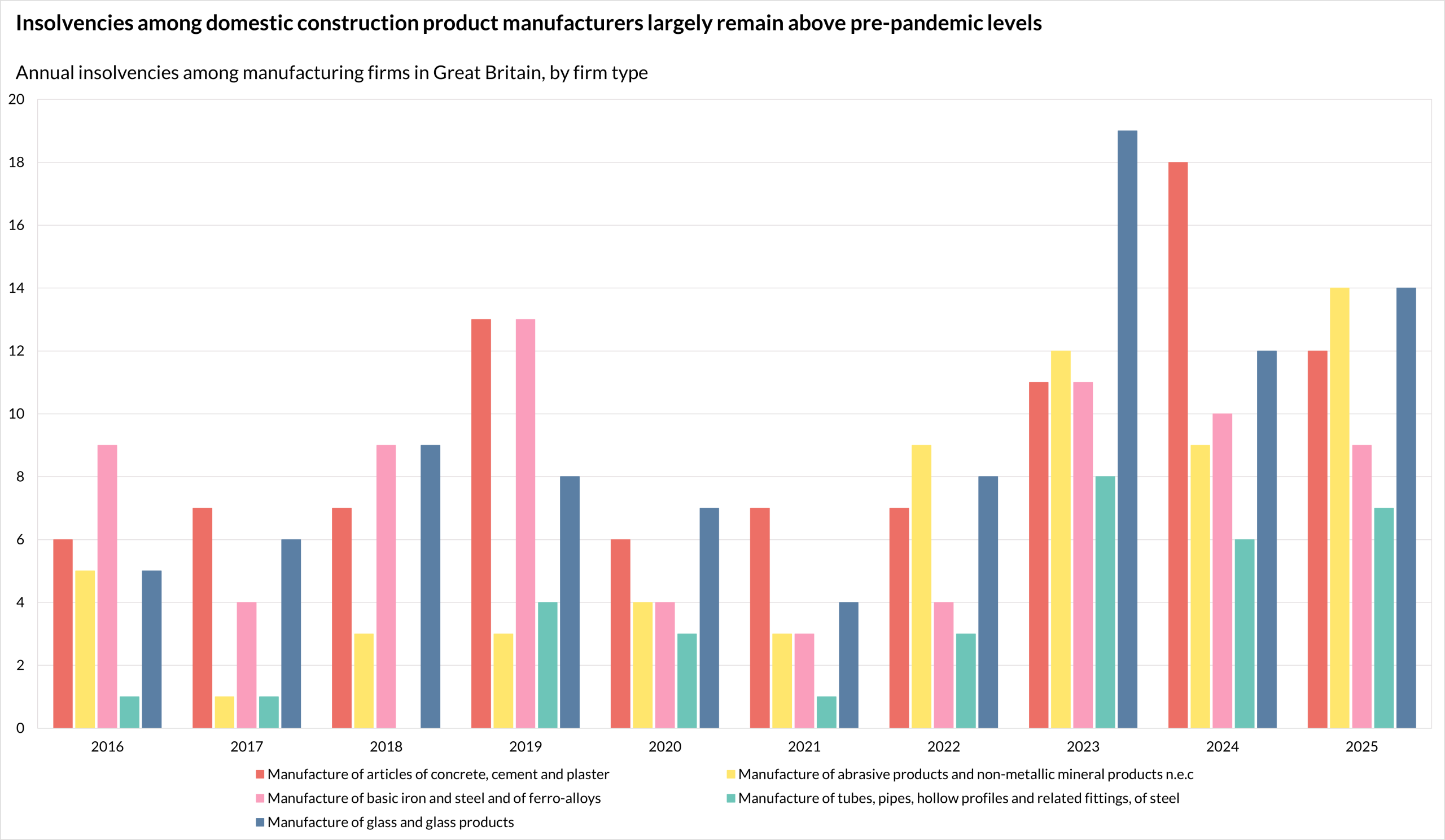

Prior to the outbreak of the recent conflict, insolvencies among UK manufacturers of non-metallic mineral products, including concrete, cement and plaster, were still elevated compared with pre-pandemic levels. In other words, there is existing fragility in the domestic supply base.

Source: The Insolvency Service – Company Insolvency Statistics January 2026, Table 1c

Encouragingly, government policy is increasingly seeking to support domestic production. In steel, higher tariffs on imports from July 2026 are intended to reduce reliance on overseas supply and redirect demand toward domestic suppliers.

However, there is concern that this could increase input costs for construction, with potentially negative implications for contractor margins, project viability and demand for products and materials as a result.

A clearer priority for government may be to support sustained construction demand, as this remains a primary driver of supplier stability.

At present, demand appears weak across several sectors. BCIS downgraded its five-year forecast for new work output growth to 12% between 2026 and 2031. In addition, BCIS polling in late March of more than 350 construction professionals – the majority cost consultants and surveyors – found that 24% expect their workload to decline in the next 12 months, while 43% anticipate no change.

Weaker demand expectations translate into reduced production forecasts for suppliers.

Made UK’s Manufacturing Outlook report for 1Q2026(5) forecast a 0.2% increase in output in the non-metallic minerals segment in 2026 – a weaker outlook than in the previous quarter.

The report notes that output in this segment is closely linked to construction and infrastructure activity, including the supply of bricks, glass and aggregates, with future performance expected to depend on the government’s delivery of planned investment.

Managing the effects of current volatility alone may not be sufficient to support future supply chain resilience. After all, energy markets are largely outside the direct control of government and industry.

However, policy can influence construction demand and cost pressures. With the conflict showing no sign of abating, removing barriers to construction investment and easing manufacturing costs may be the most effective way to stabilise domestic supply in the long term.

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.

(1) Department for Business and Trade – Building materials and components statistics: February 2026 – here

(2) Office for National Statistics – Output in the construction industry – here

(3) MPA – Four years of decline in British construction demand threatens jobs and future capacity, warns MPA – here

(4) UK Parliament – Gas and electricity prices during the ‘energy crisis’ and beyond – here

(5) MPA – Manufacturing Outlook 2026 Q1 – here