The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance. If you would like to speak with the team call us +44 0330 341 1000, email contactbcis@bcis.co.uk or fill in our demonstration form

Published: 31/03/2026

Although price inflation in construction materials has moderated since the global energy crisis four years ago, underlying risks remain amid evolving global pressures. BCIS chief economist Dr David Crosthwaite explores recent data trends and assesses whether construction materials prices have really stabilised.

Are higher construction materials prices the new normal?

Conflict in the Middle East has nearly continued beyond the four-to-six-week period initially indicated by the White House, with longer-term implications and disruption for UK construction now likely.

Materials prices are one area of pressure. Although prices have eased from the peaks seen after the energy shock linked to Russia’s invasion of Ukraine, they remain above pre-pandemic levels and are expected to come under further upward pressure in months to come.

BCIS polling of more than 350 construction professionals, the majority cost consultants and surveyors, in late March found that almost all respondents (95%) expected materials costs to rise over the next 12 months. By comparison, 62% anticipated a rise in labour costs.

Recent data from the Department for Business and Trade (DBT) and the Office for National Statistics (ONS) provide useful benchmarks for assessing current materials price movements in a historical context.

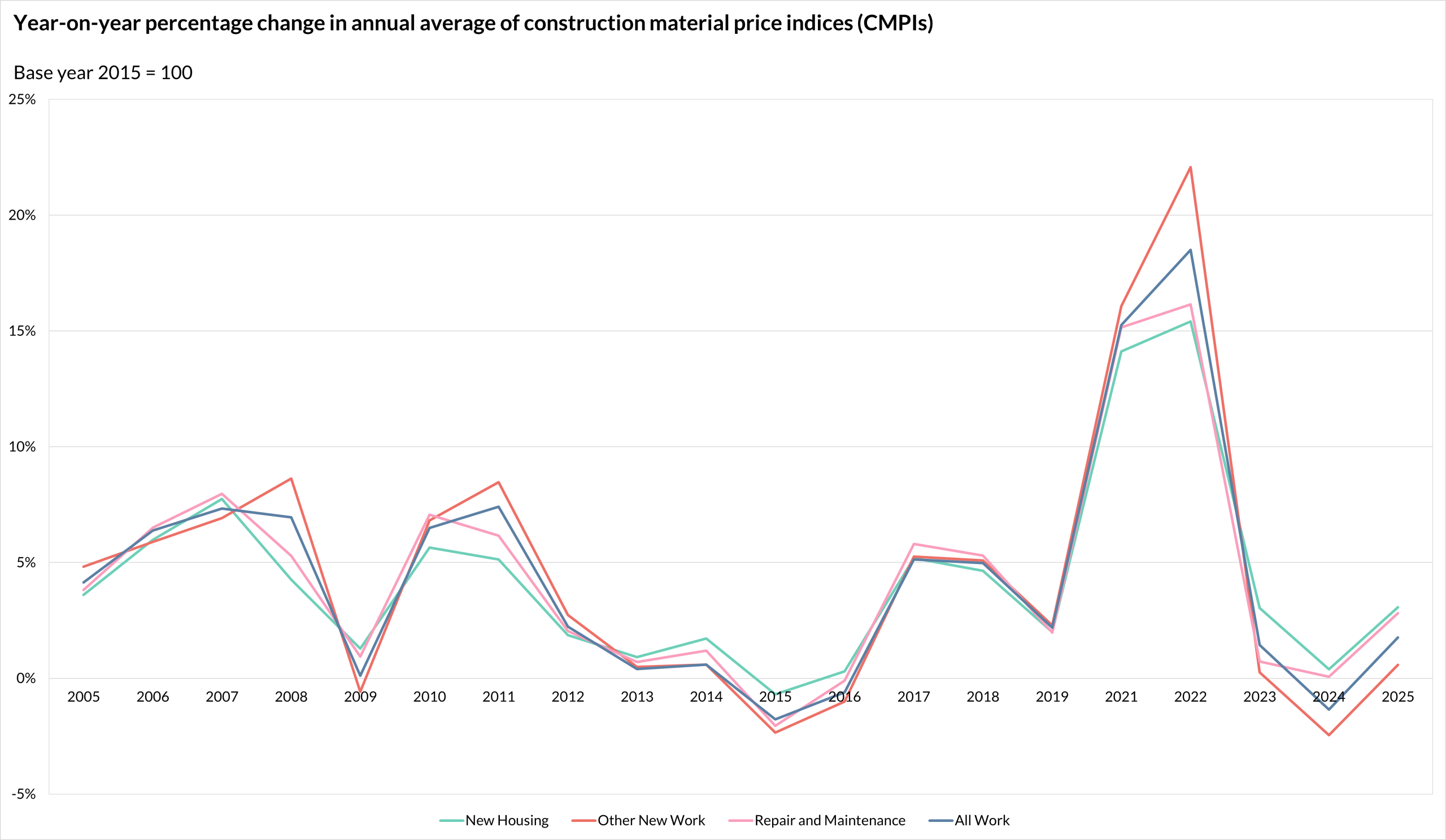

In 2025, the annual average of DBT’s All Work index, which measures changes in a range of works across sectors based on weighted resource cost indices, rose by 1.8% year-on-year. The index, which is one of four construction material price indices (CMPIs) compiled by BCIS on DBT’s behalf(1), was 39.1% higher than its pre-pandemic level in 2019(2). Compared with ten years ago, the index increased by 55.9% and was more than double its level in 2005.

These trends indicate that materials prices have generally continued to rise and they now maintain a much higher base than the level observed before Russia’s invasion of Ukraine.

Source: Department for Business & Trade – Building materials and components statistics, Table 1b

While the CMPIs tend to follow similar trajectories, the Other New Work index appears to react more sharply to economic shocks and may reflect the infrastructure sector’s heavier reliance on steel and concrete products, where prices can be more volatile.

For example, between 2021 and 2022, the annual average of the ONS producer price indices (PPI) for concrete reinforcing steel bars and pre-cast concrete products rose by 38.0% and 25.7% respectively.

Source: Department for Business & Trade – Building materials and components statistics, Table 2

Looking at past trends, it wouldn’t be surprising to see current geopolitical tensions trigger similar spikes that could potentially push prices to an even higher plateau. The problem with this is twofold.

Confidence has only just started to stabilise again after US tariff-driven uncertainty last year. Prolonged conflict, and its impact on client and business confidence, may not only dampen near-term demand for construction but also introduce a further economic shock in close succession to previous events. This could sustain higher prices, extend uncertainty and delay a recovery in UK construction and the wider economy.

Currently, market conditions seem less volatile than in the immediate aftermath of Russia’s invasion. UK wholesale gas prices briefly peaked above 170 pence per therm on 19 March(3), compared with approximately 800 pence per therm in March 2022.

However, the situation and market reactions can evolve quickly, making it important for clients and construction businesses to monitor materials price movements closely. A useful starting point is to consider where individual prices stood ahead of the current period of unrest.

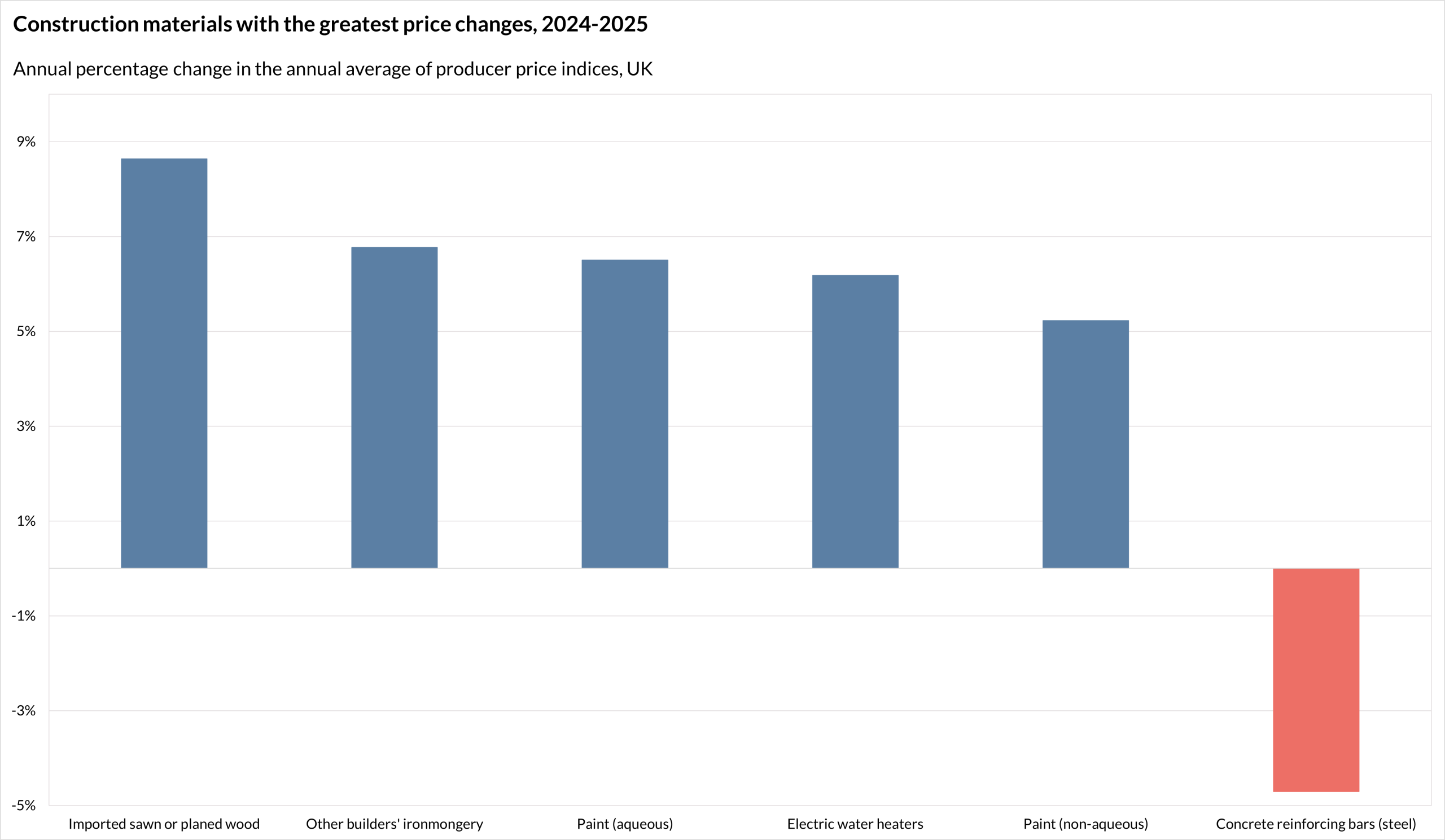

Provisional annual average PPI data show that between 2024 and 2025, imported sawn or planed wood recorded the largest increase of all materials, rising by 8.6%. This was followed by a 6.8% increase in other builders’ ironmongery. In contrast, concrete reinforcing steel bars saw the steepest decline, falling by 4.7%.

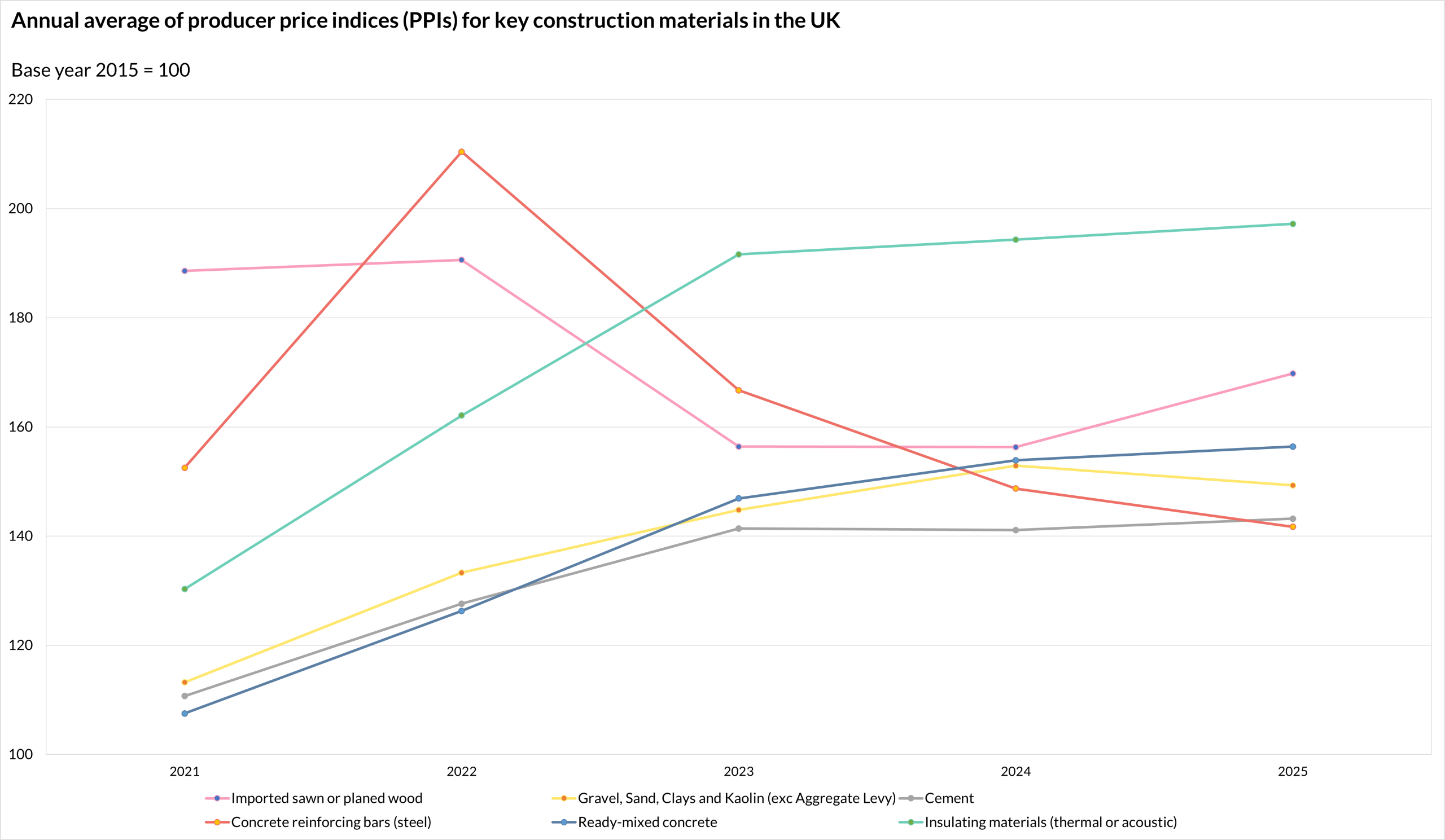

Source: Department for Business & Trade – Building materials and components statistics, Table 3

Notably, the materials that recorded the largest price increases between 2024 and 2025 differ from those that saw the most significant rises over the longer period from 2021 to 2025.

Over this timeframe, thermal and acoustic insulating materials experienced the largest cumulative increase, rising by 51.3%, while steel products, including reinforcing bars and fabricated structural steel, continued to show downward trends.

This shift is important in the context of current geopolitical tensions. It suggests that recent price movements have become more material-specific and less closely tied to the energy-related cost pressures that drove earlier increases. As a result, any longer-term disruption to energy markets arising from the Middle East conflict could alter this pattern, potentially reintroducing broader, more synchronised price pressures across construction materials.

Monthly PPI data for 2025 provide further insight into near-term movements. Across many core construction materials, monthly price changes generally ranged between a 2% increase and 2% decrease last year, although there were periods of more pronounced movement.

For example, structural materials prices showed a mid-year softening. Fabricated structural steel prices fell by 4.0% in June and by a further 2.0% in July. Concrete reinforcing steel bars also recorded consecutive monthly declines through the summer, including a 3.6% fall in June.

Alongside slower growth in some aggregate indices towards the end of the year, this mid-year easing points to weaker construction demand, consistent with industry sentiment surveys and more subdued new work output data published in late 2025. A softer demand backdrop, combined with emerging economic risks, may reduce clients’ willingness to commit to new projects.

A new joint statement(4) from John Newcomb, CEO of the Builders Merchants Federation (BMF), and Peter Caplehorn, CEO of the Construction Products Association (CPA), provides useful context. They suggest the conflict in the Middle East is unlikely to significantly affect the availability of products and materials in the UK, as these are largely produced domestically or sourced from Europe.

However, pricing remains a greater concern. Transport costs are reportedly becoming more unpredictable, and within the mechanical engineering sector, the prices of copper and steel are of particular note, consistent with findings from the latest BCIS Civil Engineering Tender Price Index Panel. The key risk is that rising materials costs will be passed on to SMEs, increasing their exposure to financial pressure and potentially insolvency.

The outlook therefore remains uncertain. Much will depend on how geopolitical tensions evolve, how long they persist and the extent to which they disrupt energy markets, although some level of disruption now appears inevitable.

Global factors will also play a role. Energy shortages are being felt more acutely in Asia, which are more reliant on Middle Eastern oil and gas. According to the BMF and CPA statement, this is now feeding through into prices, with some imported goods prices increasing by as much as 100% or more in certain cases.

With the conflict now ongoing for over a month, a higher cost base for materials may already be the new normal.

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.