The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance. If you would like to speak with the team call us +44 0330 341 1000, email contactbcis@bcis.co.uk or fill in our demonstration form

Published: 13/04/2026

Rising input costs linked to geopolitical tensions have brought materials back into the spotlight. Yet, as BCIS chief economist Dr David Crosthwaite explains, labour costs continue to exert a quieter but more lasting pressure on construction.

Materials costs may be the more immediate concern for construction clients and contractors amid ongoing tensions in the Middle East, but the direction of labour costs should not be overlooked.

Recent increases in the National Living Wage and National Minimum Wage are pushing up employment costs for many construction businesses. Beyond direct increases to base pay, such changes are also likely to have a ripple effect across pay structures as employers seek to maintain wage parity between different roles and levels of experience.

Set against a backdrop of sustained weak demand, this places additional pressure on margins and project viability, underscoring the growing importance of close collaboration between clients, developers and contractors.

Labour costs are expected to see moderate growth in the coming years, with BCIS forecasting a 15% rise between 1Q2026 and 1Q2031. Recent BCIS polling of more than 350 construction professionals, the majority cost consultants and surveyors, echoed this, with 62% predicting an uplift in labour costs in the next 12 months.

For now, these projected rises seem relatively manageable. Labour costs typically move more slowly than materials costs and, with demand currently subdued, labour availability, and therefore shortage-related cost pressures, are reportedly stable. The main exceptions, as cited by the BCIS Tender Price Index Panel, are pockets of shortages in specialist trades, such as sprinkler installation and façade works.

The greater challenge will emerge if weak demand persists and forces developers and contractors to continue absorbing higher labour costs in the long term. This is because weak demand can make tendering environments more competitive and see bidding businesses accept lower margins simply to maintain workload and cash flow.

In stronger market conditions, input cost increases are more easily passed on to clients, as demand for work exceeds available capacity. However, the higher prices clients face could be compounded by structural vulnerabilities in construction’s labour supply as contractors price in the heightened risk of shortages.

Construction’s workforce has declined over the past two decades, with both employed and self-employed numbers still below pre-pandemic levels. This has created two key challenges. First, reduced flexibility in capacity means the sector may be less able to respond quickly to spikes in demand. Second, any increase in demand is more likely to intensify competition for smaller pools of skilled workers, driving up labour costs for contractors and contributing to viability constraints or higher tender prices where cost inflation is sustained.

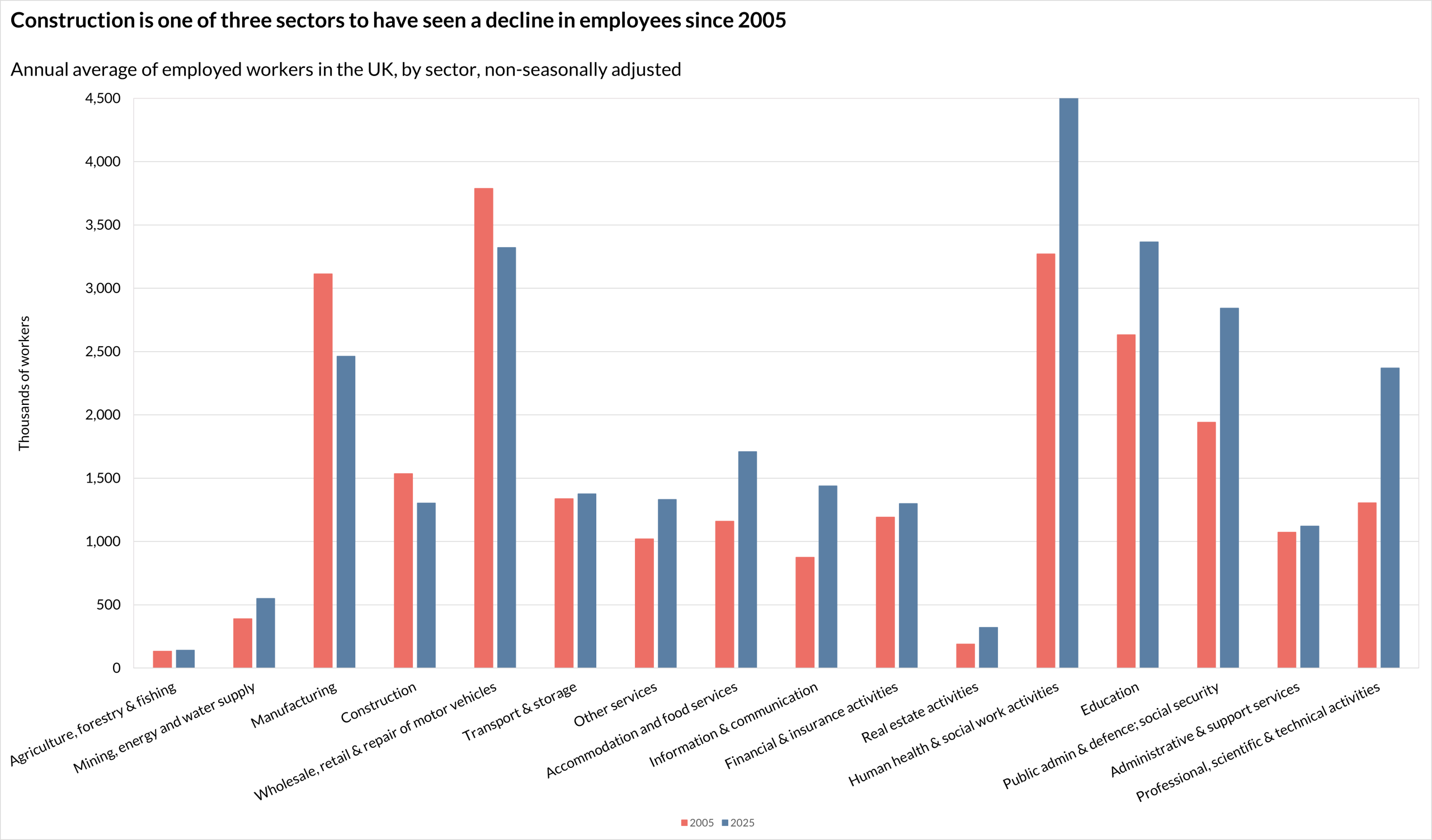

Unlike most other sectors, the size of construction’s employed workforce in 2025 was lower than every five-year benchmark since 2005, according to data from the Official for National Statistics’ Labour Force Survey(1).

Source: Source: ONS – EMP14: Employees and self-employed by industry, People Employees

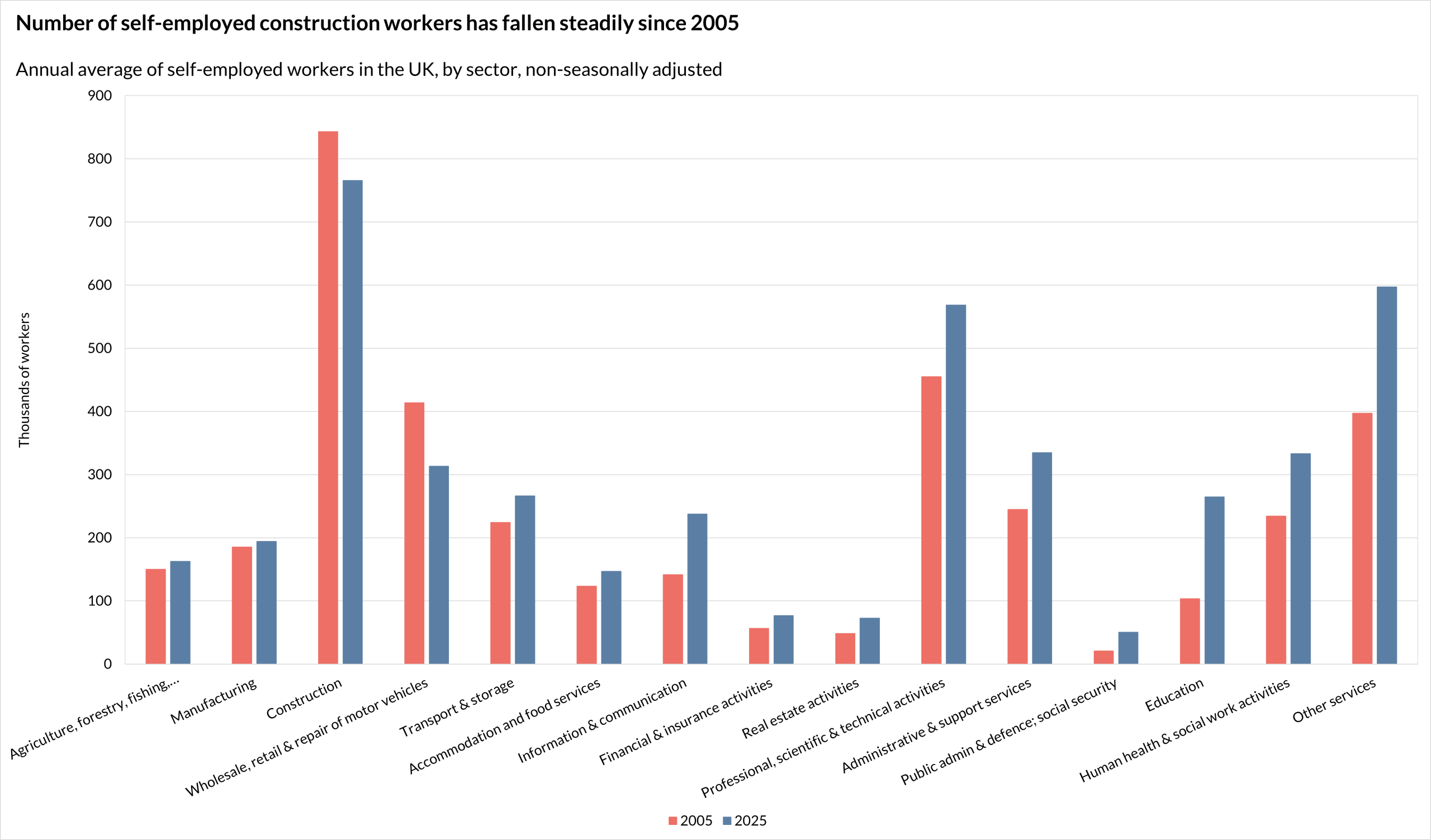

A similar trend is visible across self-employed construction workers, with the exception of a marginal 1% rise between 2024 and 2025.

Source: ONS – EMP14: Employees and self-employed by industry, People Self employed

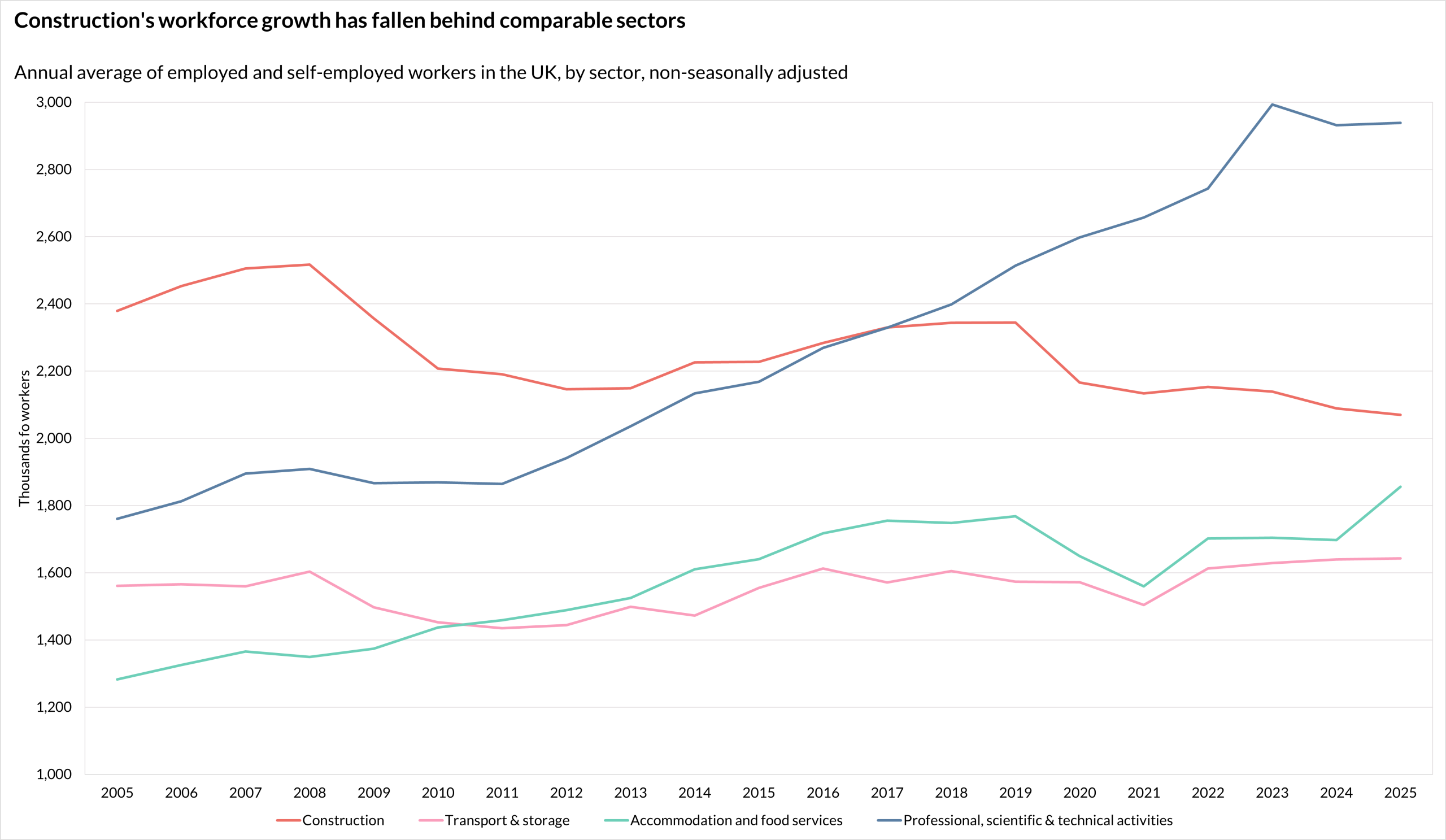

While construction’s workforce reduction may seem modest relative to long-term declines in manufacturing and wholesale, retail and motor vehicle repair, comparisons with sectors that have similarly sized workforces reveal a much more significant contraction.

Transport and storage, accommodation and food services, and professional, scientific and technical activities – all with workforces comparable in size to construction – experienced sustained growth in their total workforces (employees and self-employed) between 2005 and 2025.

Most notably, the total workforce in the professional, scientific and technical activities sector increased by 67%. By contrast, construction’s workforce shrank by 13%.

Source: ONS – Source: ONS – EMP14: Employees and self-employed by industry, People Employees and People Self employed

In part, this reflects the shift towards a knowledge-based economy and the opportunities created by technological change for sectors that rely less on intensive, manual labour. It also underscores construction’s cyclical nature and its sensitivity to economic shocks, the effects of which can prevail for many years.

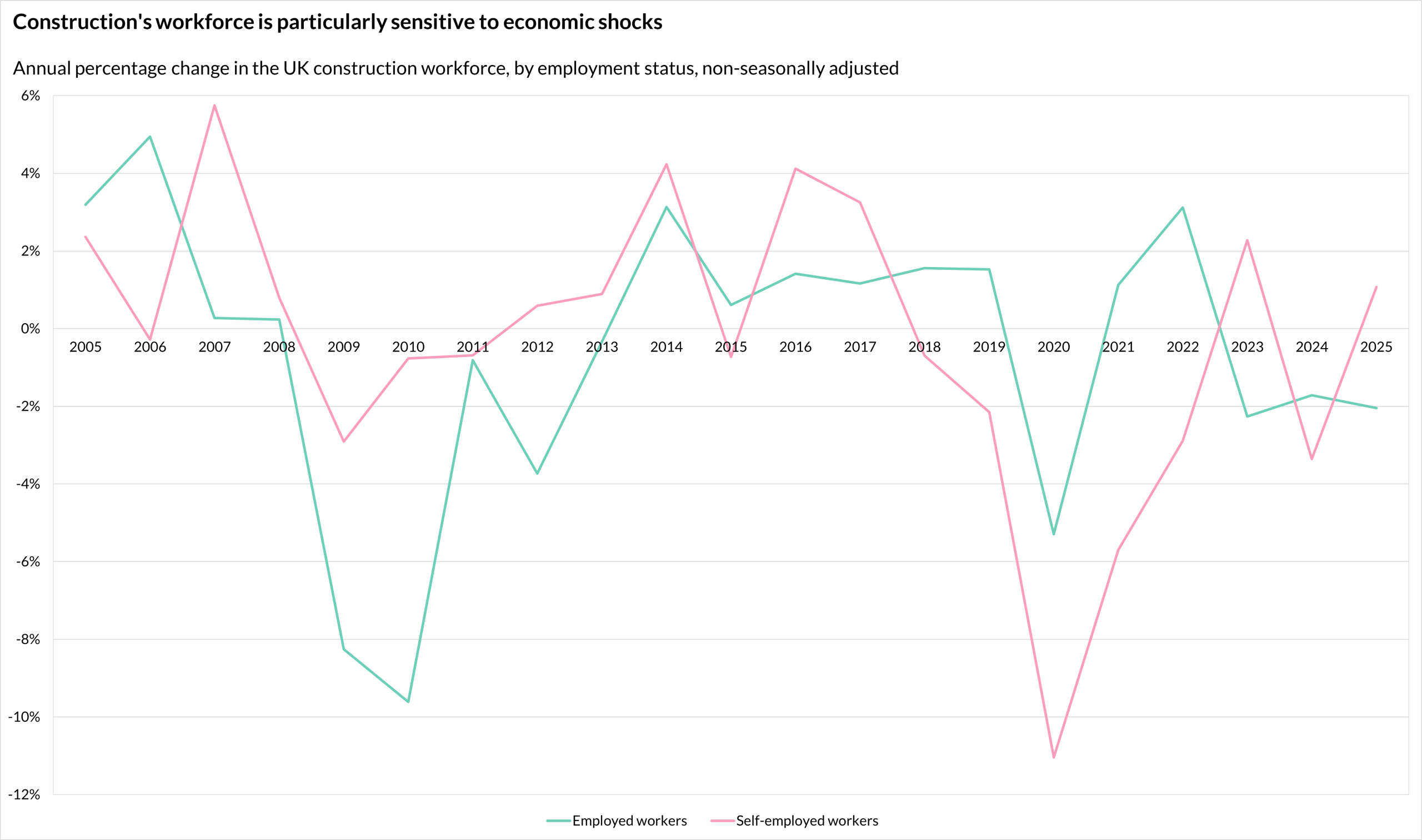

ONS data show that following the onset of the global financial crisis in 2008, construction employment fell sharply, declining by 8% year-on-year in 2009 and a further 10% in 2010. The next largest contraction in the last 20 years occurred in 2020, during the pandemic, when employee numbers decreased by 5%.

Source: ONS – EMP14: Employees and self-employed by industry, People Employees and People Self employed

By contrast, self-employed construction workers showed a different pattern. Declines were less severe during the financial crisis (3% in 2009 and 1% in 2010), but more pronounced during the pandemic, with numbers falling by 11% in 2020 and 6% in 2021.

These trends suggest that self-employed construction workers may be more resilient during traditional economic downturns, but more vulnerable to acute shocks such as the pandemic.

While current uncertainty may have less of an impact on self-employment, the reduced size of the self-employed workforce compared to previous years means that employee layoffs could intensify future capacity constraints in the wider sector.

Against a backdrop of resource fragility, the overlap between rising employment costs and ongoing disruption leaves construction in a challenging position. Whether demand stagnates or strengthens, there are cost implications, either squeezing business margins or increasing prices for clients.

For those involved in cost planning and procurement, this reinforces the importance of closely monitoring labour cost forecasts and using up-to-date indices to track and account for inflation. While materials prices remain elevated and sensitive to geopolitical shocks, recent experience shows that labour costs can continue to sustain inflationary pressure even after materials costs begin to stabilise.

Adding further complexity, insights from recent meetings of the BCIS Tender Price Index Panel highlight that demand conditions are not uniform. Growth sectors such as the data centre market are intensifying competition for key trades – particularly MEP subcontractors – creating the potential for localised labour pressures even within an otherwise subdued market.

This is likely to become a more prominent feature of the market as government policy continues to emphasise place-based investment. Growth corridors such as Oxford–Cambridge, alongside regional investment zones and mayoral funding programmes, are expected to concentrate construction activity geographically.

While this may support overall demand, it also introduces the potential for delivery constraints. Where multiple large schemes progress simultaneously within the same locations, local labour markets may struggle to respond, increasing competition for specialist skills and driving up costs, although labour mobility may help to alleviate some of these pressures.

That said, subdued demand remains the more likely scenario overall. Renewed Israeli strikes in Lebanon, failed talks over Iran’s nuclear ambitions and the US’s blockade of the Strait of Hormuz have raised doubts about the possibility of a resolution to the conflict in the near term.

In this confidence-sapping environment, contractors may face increased pressure to absorb cost risk in order to secure work, with mechanisms such as fluctuation clauses and index-linked adjustments increasingly used to manage uncertainty.

Ultimately, the key challenge for the sector is not focusing on either materials or labour cost movements, but recognising that both may act together. Materials may drive short-term volatility, but minimum wage increases, uneven demand and skills shortages mean labour will continue shaping the longer-term cost base of construction.

For clients and contractors alike, this reinforces the need for more proactive cost planning, greater collaboration and a clearer understanding of how labour market constraints could influence pricing, procurement and project viability in the years ahead.

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.

(1) Office for National Statistics – EMP14: Employees and self-employed by industry – here