The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance. If you would like to speak with the team call us +44 0330 341 1000, email contactbcis@bcis.co.uk or fill in our demonstration form

Published: 21/07/2026

EY-Parthenon publishes its profit warnings report on a quarterly basis(1). The report outlines the profit warnings issued by FTSE companies across different sectors and provides analysis on the driving factors behind them.

Profit warnings are statements issued to the stock exchange by listed companies to declare that their full-year profits will be materially below management or market expectations.

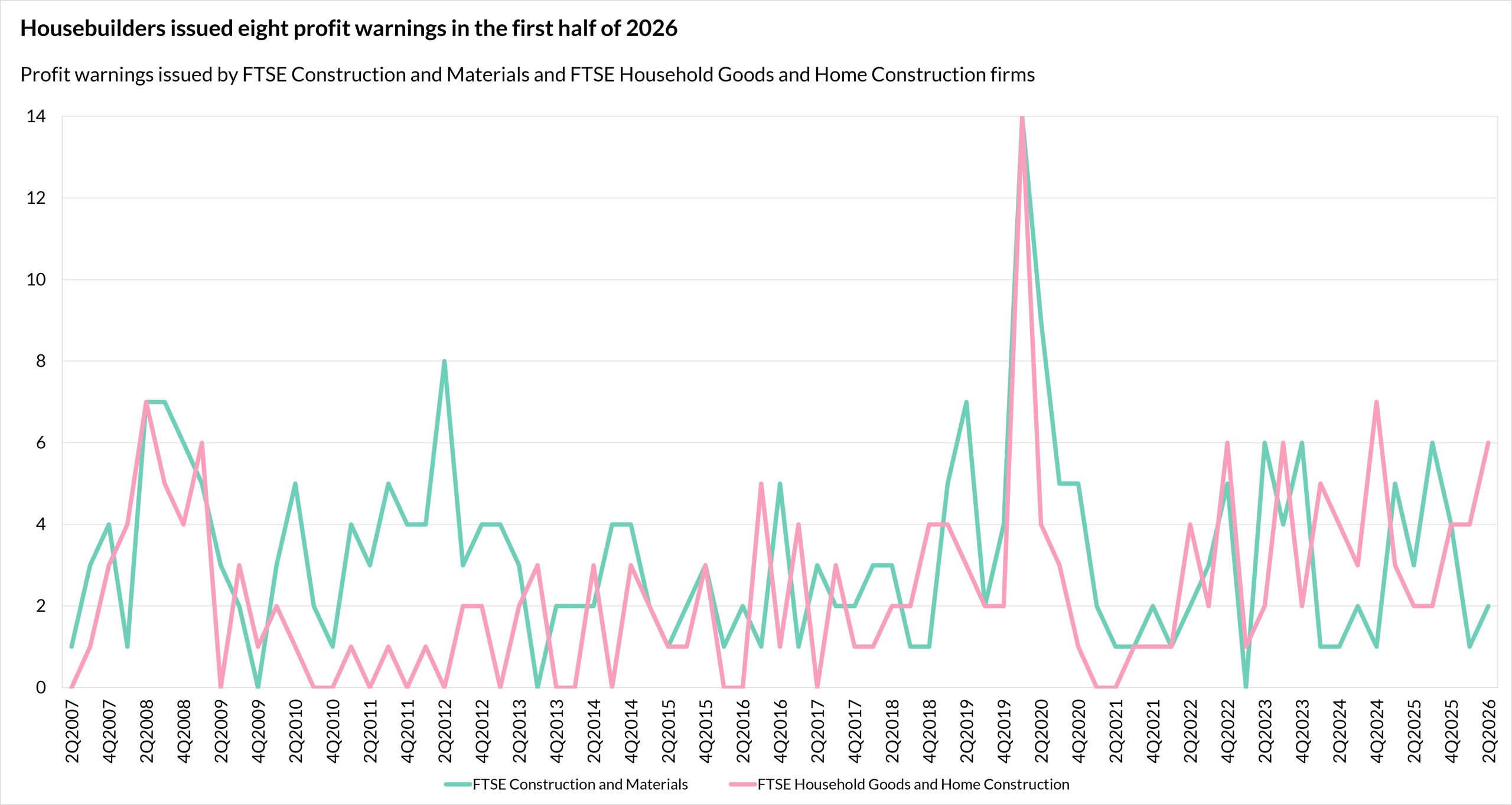

Housebuilder profit warnings surge in second quarter

FTSE Household Goods and Home Construction companies, which include housebuilders, issued six profit warnings in the second quarter of 2026, according to new analysis by EY-Parthenon.

This was up from four in the first quarter, taking the sector total for the first half of 2026 to ten. Eight of these came from housebuilders alone, matching the peak reached during the global financial crisis in 2008.

Elsewhere, FTSE Construction and Materials companies issued two profit warnings in the second quarter compared with one in the first.

Source: EY-Parthenon, Analysis of UK Profit Warnings

In the 12 months to the end of the second quarter, the FTSE Household Goods and Home Construction sector recorded the highest proportion of companies issuing profit warnings of any FTSE sector, at 58%.

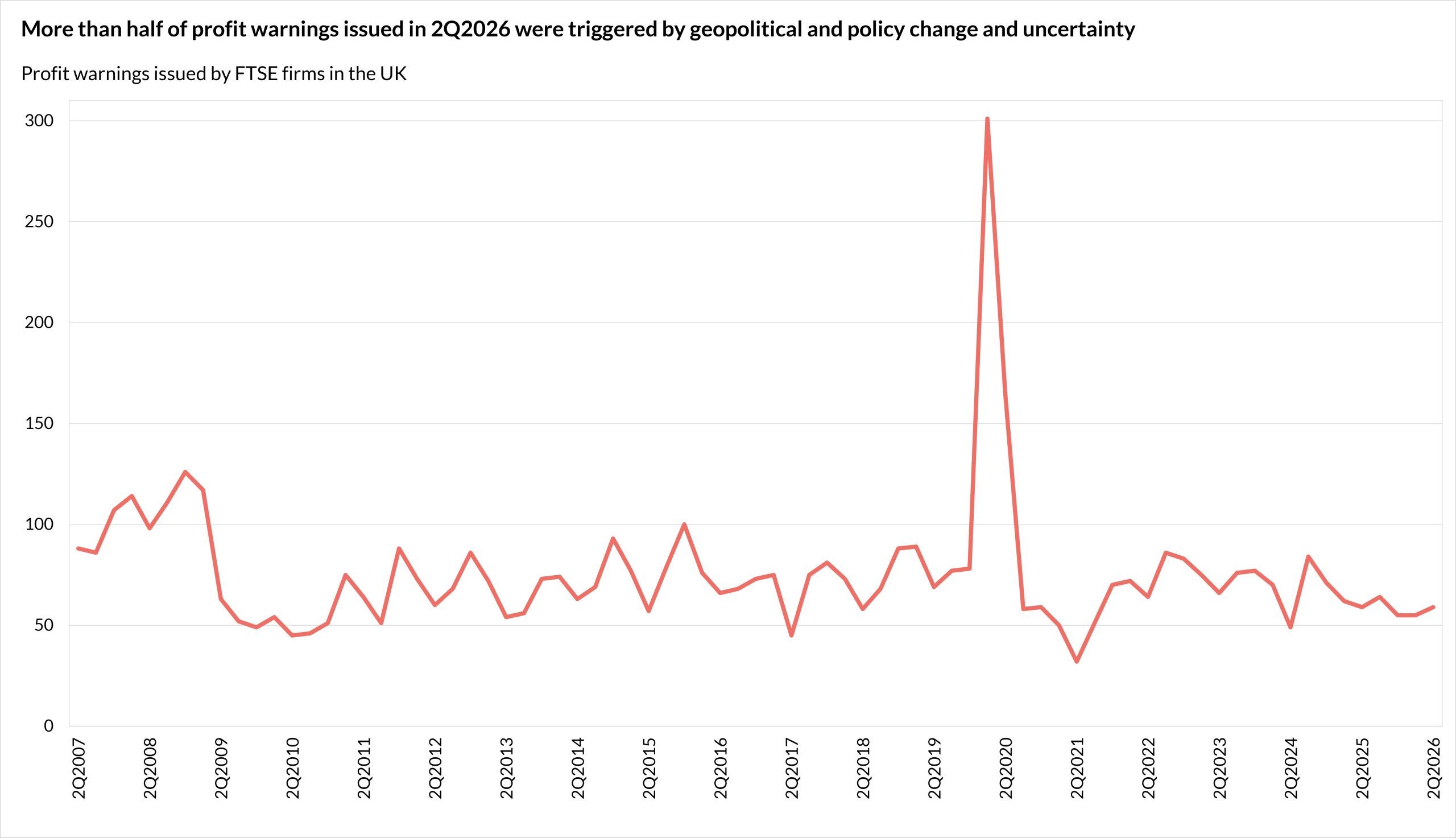

Across all FTSE sectors, 59 profit warnings were issued during the second quarter of 2026. The most frequently cited triggers for warnings were geopolitical or policy change and uncertainty (53%), rising costs and overheads (27%), delayed or cancelled orders (25%) and weaker consumer confidence (14%).

Source: EY-Parthenon, Analysis of UK Profit Warnings

Dr David Crosthwaite, chief economist at BCIS, said: ‘New profit warnings data are another bell tolling for the government’s 1.5 million homes target. Under the heavy weight of taxes, regulation and a growing range of cost pressures, including those stemming from the Middle East conflict, housebuilding is becoming a hamstrung business.

‘Burnham’s council housebuilding vision has some merit, but in practical terms the task is monumental. The cost of establishment, for instance, would likely be significant and that’s before building even starts.

‘Inflationary pressures on materials and fuel remain a concern too, particularly while tensions in the Middle East continue to create uncertainty in global energy markets. If the government is serious about meeting its housing ambitions, it needs to make development more viable for both public and private housebuilders.

‘Actions within its control include reviewing the cumulative burden of levies and regulatory costs placed on development. The Building Safety Levy, for example, serves an important purpose, but ministers should ask whether there is a better way to fund it. If shifting the burden helps unlock housing delivery without compromising building safety, it could prove a worthwhile trade-off.

‘The next biggest priority is supporting demand. While interest rates sit largely in the hands of the Bank of England, ministers still have levers they can pull to improve affordability and boost buyer confidence. Measures that support first-time buyers would likely make a meaningful difference.

‘This is starting to feel like the last chance saloon for this Parliament to get the UK’s housing sector back on track. Difficult trade-offs will undoubtedly be required, but if they strengthen growth and improve access to housing, they are worth making.’

In its commentary, EY-Parthenon noted that UK-listed housebuilders have issued 47 profit warnings since the start of 2020, almost double the 27 recorded over the previous 13 years combined. Many entered 2026 expecting a gradual recovery, but trading conditions have remained challenging.

Explaining the latest warnings from FTSE Household Goods and Home Construction companies, EY-Parthenon said the escalating conflict in the Middle East created fresh headwinds. Higher energy and input costs, weaker consumer confidence and fading expectations of near-term interest rate cuts have all weighed on the sector.

Although visitor numbers and buyer enquiries have shown some improvement, this has yet to translate into a sustained increase in reservations or completions. Meanwhile, measures to stimulate sales, including mortgage contributions, deposit support and part-exchange schemes, have come at the expense of profit margins.

EY-Parthenon remained optimistic about the sector’s longer-term prospects, citing persistent housing shortages, supportive government policy and expectations of lower interest rates from 2027 as factors that should underpin demand.

However, it warned the near-term outlook remains difficult. Traditional self-help measures, such as disposing of land at attractive values or refinancing debt, have become harder to execute. Investor caution and uncertainty surrounding Building Safety Act liabilities are also continuing to constrain refinancing and merger and acquisition activity.

Looking at the broader economic outlook, Jo Robinson, EY-Parthenon Head of UK & Ireland Turnaround and Restructuring Strategy, said the stabilising of headline profit warning numbers masks a changing and challenging underlying picture.

‘Many companies will adapt and thrive. But there is growing evidence that years of rolling disruption have eroded corporate resilience. Restructuring activity is rising, with stress becoming more concentrated in sectors most vulnerable to changing cost, confidence and credit conditions,’ she said.

‘This is the most relentless profit warning cycle recorded in the 25-year history of this survey. The number of profit warnings is stabilising, but the proportion of listed companies issuing warnings has hit levels more typically associated with recession in six of the last seven years.

‘Whilst no single shock has matched the severity of the global financial crisis or pandemic, the cumulative impact of successive disruptions could be just as powerful.’

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.

(1) EY-Parthenon – Analysis of UK profit warnings – here