The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance.

Published: 24/03/2026

The arrival of the government’s new Steel Strategy has provided welcome clarity and direction for the UK steel industry, but ongoing geopolitical instability could limit its impact.

The strategy sets out a range of measures designed to strengthen the domestic steel industry, including a commitment to double tariffs on foreign steel imports from July 2026.

Import quotas will be reduced by 60% and any steel arriving in the UK above these levels will be subject to a 50% tariff.

BCIS chief economist Dr David Crosthwaite said that while the strategy represents a more defined policy approach to addressing long-standing issues in domestic steel, new measures may not be enough to fully offset the impact of conflict in the Middle East.

‘Competition from cheaper steel imports poses an immediate threat to domestic producers. The new Steel Strategy and pledge to impose higher tariffs on foreign steel from July are bold steps towards tackling this challenge,’ he said.

‘However, significant risks remain. While new quotas on foreign steel are reportedly designed to maintain supply and limit wider economic disruption, securing the future of the domestic steel industry has become more complex amid renewed geopolitical tensions.

‘In short, although tariffs may help to reduce reliance on imports, volatility in energy markets could continue to weigh heavily on domestic steel producers by driving up production costs, particularly ahead of the British Industrial Competitiveness Scheme rollout. Geopolitical uncertainty also risks dampening construction activity, and potentially steel demand as a result, should clients and funders scale back investment in a more unstable environment.’

Industry reactions to the Steel Strategy were mixed, ranging from praise for its potential impact on local economies to suggestions that tariffs may hit infrastructure projects with a cost shock.

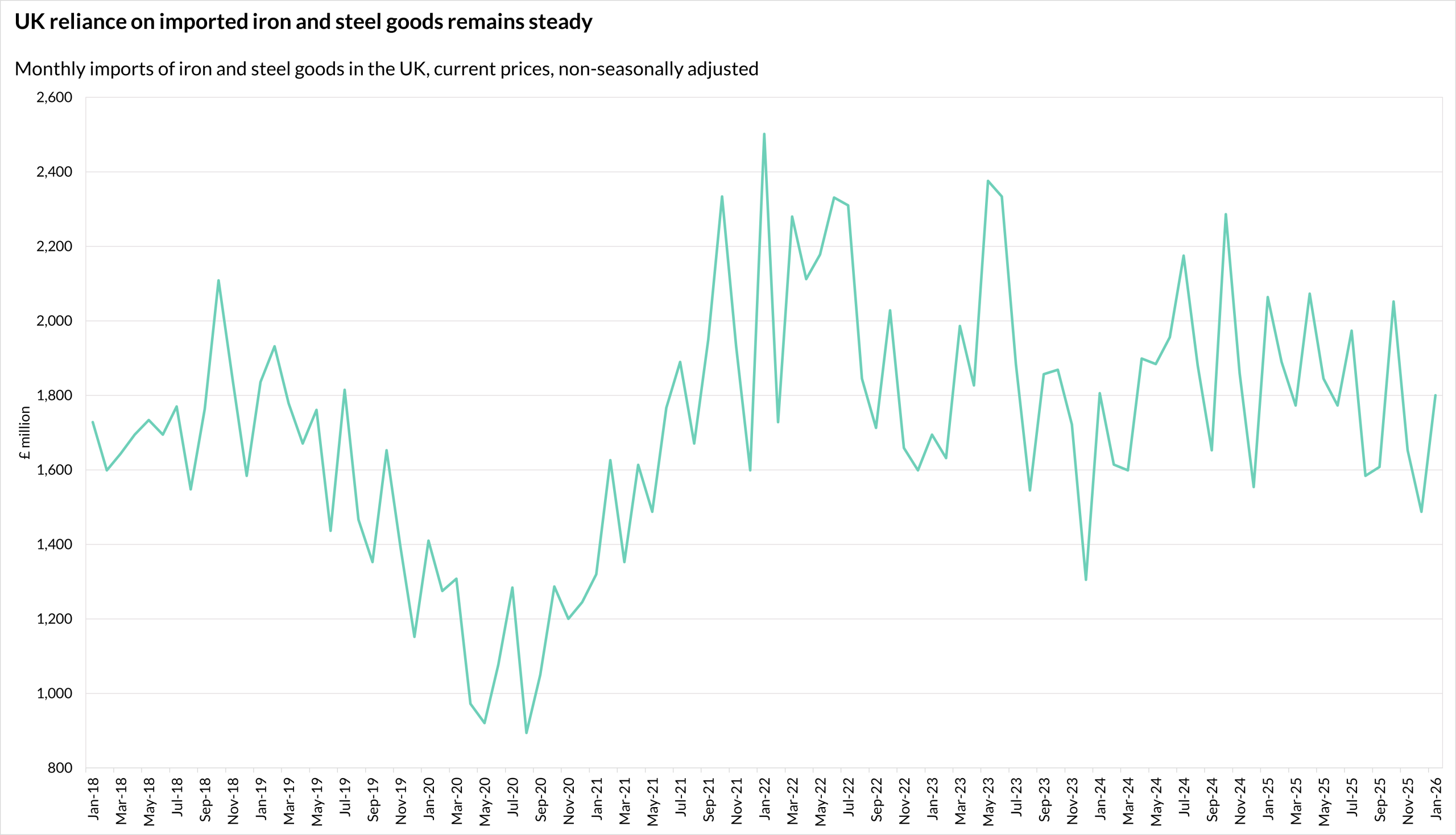

The latest data from the Office for National Statistics(1) show the UK imported £21.8 billion worth of iron and steel goods in 2025. This was down 1.8% on imports in 2024 but was an increase of 13.1% compared with 2019.

Source: ONS – Trade in goods: country-by-commodity imports, Table 3

Alongside tariff changes, the new Steel Strategy confirms plans to invest up to £2.5 billion in supporting, rebuilding and modernising the UK steel industry. The government also outlines an ambition for 40% to 50% of domestic steel demand to be met by UK production.

Further measures include a focus on electric arc furnaces as part of future steelmaking, enabling offshore wind developers to include steel manufacturers in Clean Industry Bonus applications and establishing a cross-government group to support scrap metal supply.

To keep up to date with the latest industry news and insights from BCIS register for our newsletter here.

(1) Office for National Statistics – Trade in goods: country-by-commodity imports – here