The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance.

Published: 02/04/2026

The Construction Leadership Council’s Material Supply Chain Group (MSCG) has called for collaborative working across the supply chain, as escalating tensions in the Middle East move beyond short-term market reaction into something more structurally significant.

Earlier developments were reflected largely through volatility in oil prices. More recent events point to disruption across parts of the global energy system, particularly in production, refining capacity and transport routes.

Recent incidents, including attacks on commercial shipping in the Gulf, underline that disruption is also affecting physical supply routes, as well as infrastructure.

In a statement(1) from the MSCG’s co-chairs, John Newcomb, CEO of the Builders Merchants Federation, and Peter Caplehorn, CEO of the Construction Products Association, the group this week reported there is ‘clear evidence’ that suppliers are being affected by rising fuel costs, alongside increasing volatility in shipping and delivery times. The group has encouraged early sharing of requirements across the industry to help manage uncertainty and maintain project delivery.

David Crosthwaite, chief economist at BCIS, said: ‘For construction, the nature of the disruption shapes how it feeds through. Price movements driven by uncertainty can unwind quickly if conditions stabilise. Damage to infrastructure and ongoing disruption to transport routes, however, are slower to resolve and can influence the cost environment over a longer period.

‘Beyond the market reacting to geopolitical risk, there is increasing evidence of disruption to the physical supply of energy, which changes both the scale and the potential duration of the impact.’

From volatility to supply constraints

Energy markets remain sensitive to geopolitical developments, but recent reporting suggests that damage to production facilities and refining capacity is beginning to constrain supply more directly.

At the same time, disruption to shipping routes is adding further pressure. Attacks on vessels operating near the Strait of Hormuz highlight the ongoing risk to energy transport flows, reinforcing upward pressure on both prices and insurance costs.

Dr Crosthwaite said: ‘If refining capacity is disrupted, the effects can be felt more quickly across the economy. It is not just about the price of oil, but the availability and cost of the fuels that underpin transport and logistics.’

Why this matters for construction

Energy costs are embedded throughout the construction supply chain, influencing the production, transport and delivery of materials.

Diesel prices are a key exposure. Construction activity relies on diesel-powered plant, machinery and site transport, while logistics networks depend on fuel to move materials between suppliers and sites. Changes in fuel costs can therefore feed through relatively quickly into both material prices and project delivery costs.

The impact is already being felt across transport and distribution. The MSCG reported petrol and diesel price increases of around 10% and 20% respectively in late March, with little indication that these have stabilised. Even if hostilities ease, these pressures are expected to persist in the near term.

Energy-intensive materials such as steel, cement, bricks, glass and aluminium are also exposed. These effects typically emerge with a lag, particularly where manufacturers have hedged energy costs in advance. However, sustained increases in energy prices place upward pressure on manufacturing costs once those protections unwind, which are then reflected in supplier pricing.

Shipping disruption and supply chain pressure

Shipping routes are another key transmission channel. Disruption in the Middle East has led to rerouting of vessels, with knock-on effects for cost and delivery times.

The MSCG highlighted that rerouting around the Cape of Good Hope has driven container costs up, reportedly, between 20% and 100%, alongside longer delivery times. This combination of cost volatility and delay is already affecting procurement across parts of the supply chain.

The Drewry World Container Index, which tracks the average freight costs of 40-foot containers via eight major routes, increased by 20% between 26 February, just before US and Israel air strikes on Iran, and 26 March.

Despite these pressures, availability remains relatively stable across most product groups. The majority of materials used in UK construction are sourced domestically or from Europe, limiting direct exposure to supply shortages. However, the MSCG reports where disruption is occurring, such as in imports of tiles and stone from India due to gas shortages, alternatives are available but at higher cost.

A more persistent shock?

The duration of the disruption remains uncertain. In previous energy shocks, markets have adjusted through increased production, rerouting of supply and the use of strategic reserves.

Where infrastructure has been damaged, recovery tends to take longer. Rebuilding production or refining capacity is complex, and even partial disruption can constrain global supply for an extended period.

This comes at a point when markets are approaching the end of the White House’s initial estimate of a four to six week disruption window. If supply constraints persist beyond this period, expectations will shift from short-term disruption to a more sustained tightening of global energy supply.

The potential for further escalation, including direct military involvement in securing energy infrastructure and shipping routes, introduces additional uncertainty around both the duration and severity of supply disruption.

Dr Crosthwaite said: ‘Even if tensions ease, the impact on supply may persist. That creates a different set of risks for the construction sector, particularly in terms of cost planning and procurement over the coming months.

‘There are mechanisms that may moderate price increases, including spare production capacity in other regions and the potential release of strategic petroleum reserves. These measures tend to provide short-term relief rather than a long-term solution, and may introduce further volatility as reserves are replenished.’

Timing and transmission

In the near term, markets are likely to remain volatile as expectations shift in response to political developments. The more relevant issue for construction is how conditions evolve over the next few months.

If supply constraints persist into the second quarter of the year, cost pressures could begin to emerge more clearly across fuel, logistics and eventually materials.

Wider economic conditions remain a counterbalance. Slower growth and softer demand may limit the extent to which cost increases are passed through, particularly in more competitive parts of the market.

Implications for cost planning

The current environment reinforces the importance of managing uncertainty within cost planning and procurement strategies. Projects with longer timelines may be more exposed to shifts in the cost environment, particularly if supply constraints persist.

Allowances for inflation and risk may require careful consideration. Contractors may also seek to manage exposure through pricing strategies, tender validity periods or contractual mechanisms that reflect potential volatility.

There are also emerging concerns about how costs are being passed through the supply chain. The MSCG noted that merchants, contractors and housebuilders are increasingly concerned about the rapid introduction of surcharges with limited notice or supporting evidence, adding further uncertainty to project pricing.

With costs rising at multiple points in the supply chain, margins are coming under pressure across the industry – increasing strain on contracting tiers, with smaller firms particularly exposed.

Dr Crosthwaite said: ‘The key issue is not necessarily an immediate step change in construction costs, but the potential for a more uncertain and volatile pricing environment. That is where the real challenge lies for the industry.’

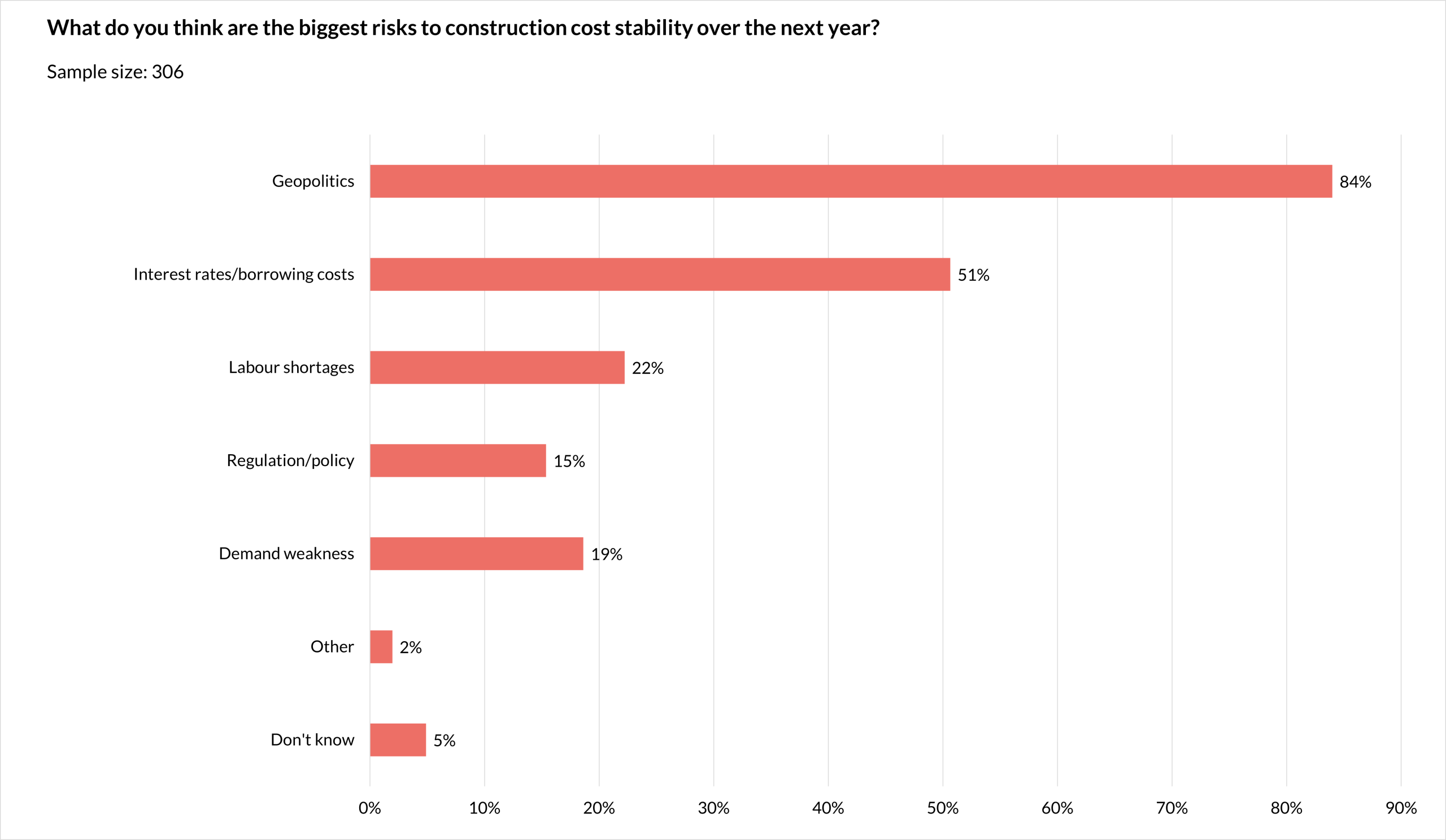

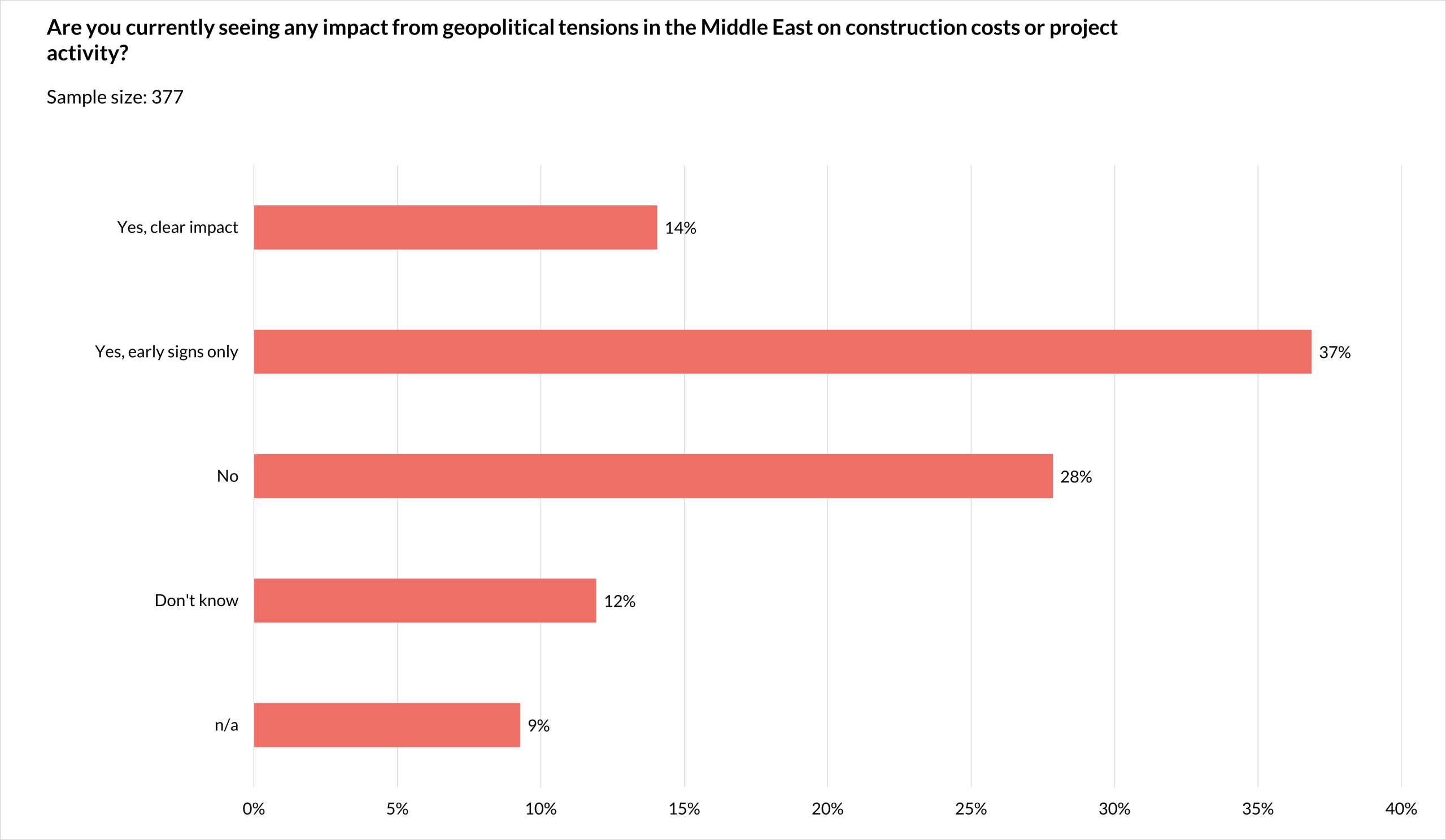

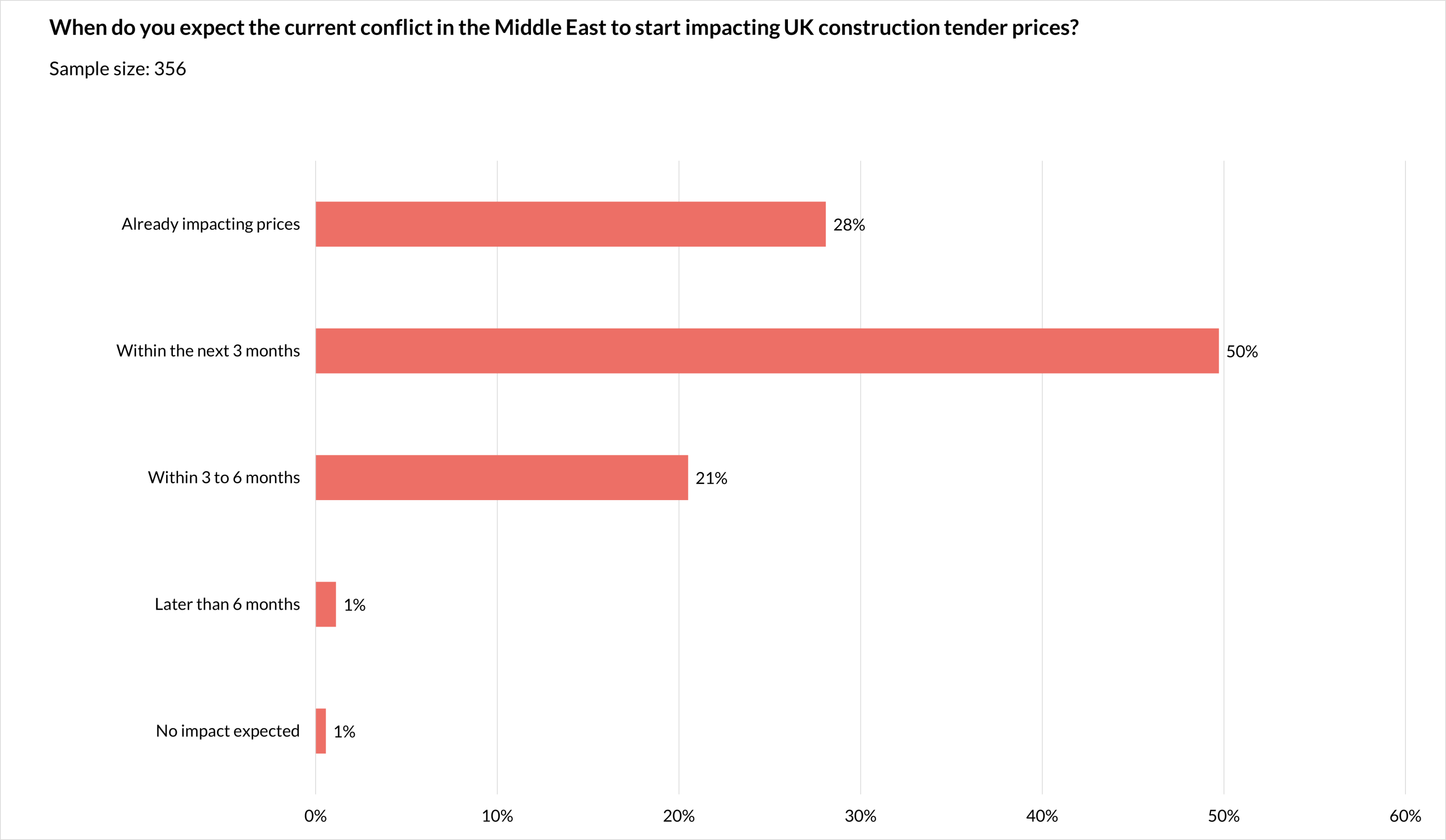

What you said

During our latest Construction Outlook webinar, we asked more than 300 construction professionals about the early effects of geopolitical tensions on the industry.

To keep up to date with the latest industry news and insights from BCIS register for our newsletter here.

(1) Material Supply Chain Group – here