BCIS CapX provides a comprehensive, detailed and easy-to-use method of measuring cost movement for building and civil engineering. Widely used in the construction and infrastructure sector to help fairly allocate risk between the client and sub-contractors.

Published: 03/07/2026

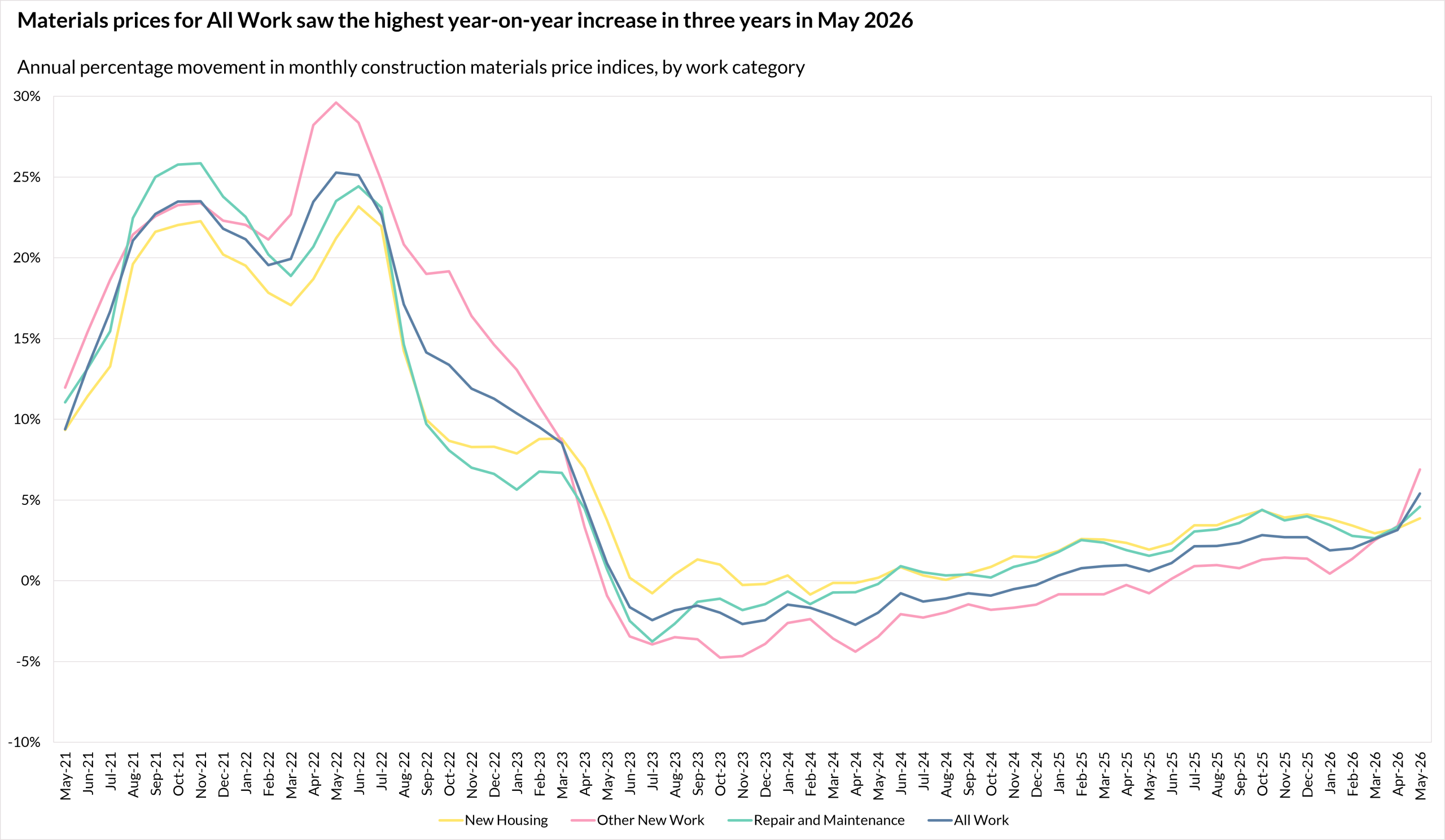

Each month the Department for Business and Trade (DBT) publishes construction materials price indices (CMPIs), categorised under All Work, New Housing, Other New Work and Repair and Maintenance, as well as tracking a selection of building materials and components for the UK(1). BCIS data is used in the compilation of the DBT indices(2).

Fabricated structural steel prices top the sharp increases recorded in May

Construction materials prices for All Work rose by 5.4% in the 12 months to May 2026, according to the latest provisional data published by DBT.

New Housing recorded a 3.9% increase while Other New Work rose by 6.9%, and Repair and Maintenance increased by 4.6% when comparing May 2026 with May 2025.

DBT’s CMPIs are compiled using a combination of resource cost indices produced and published by BCIS. These are based on BCIS Price Adjustment Formulae Indices (PAFI).

Source: Department for Business and Trade – Building materials and components statistics, Table 1a

Dr David Crosthwaite, chief economist at BCIS, said: ‘The sharper rise in materials price inflation indicated by the latest DBT indices reflects substantial price increases across a number of key construction products. Fabricated structural steel, aggregates and bituminous mixtures all recorded stronger annual increases than in recent months, suggesting that the wider impacts of higher energy costs and ongoing supply chain disruption are now feeding through into the official data.

‘The results are consistent with what we have been expecting and are beginning to show more clearly which products are experiencing the greatest inflationary pressures.

‘Higher inflation is clearly unwelcome, but the latest data provide a stronger evidence base for decision making. Rather than relying solely on expectations of future price movements, those involved in cost planning can now use observed market trends to inform estimates, budgets, procurement strategies and contract negotiations. As these trends become more firmly established in official data, they will provide greater confidence in construction cost forecasting and help the industry respond more effectively to changing market conditions.’

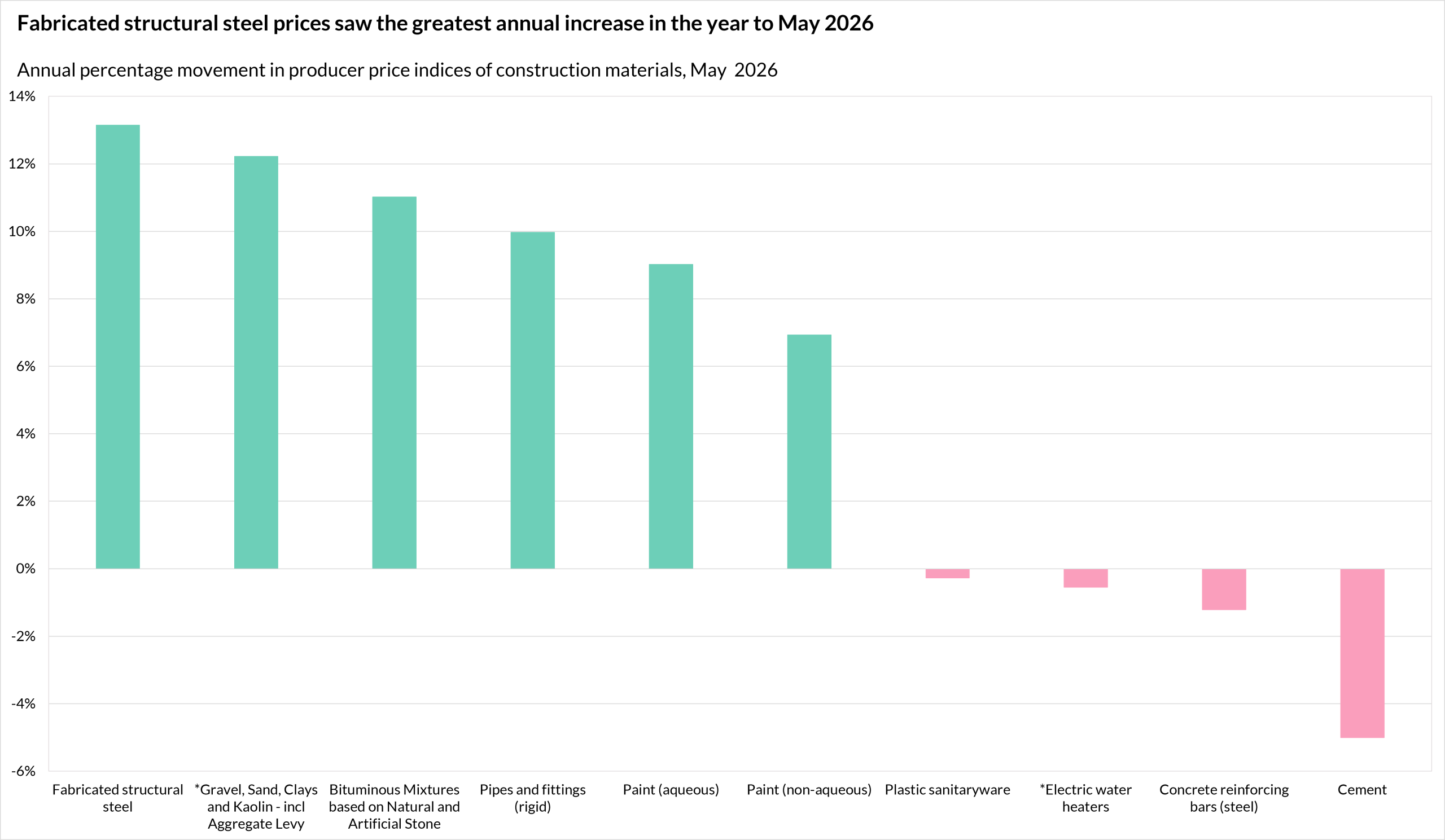

DBT data show that prices for fabricated structural steel recorded the greatest inflation in the 12 months to May 2026, up by 13.1%. This was followed by a 12.2% rise in prices for gravel, sand, clays and kaolin (including the Aggregate Levy).

Prices for cement saw the steepest annual decrease of all resources measured with a 5.0% fall.

Source: Department for Business and Trade – Building materials and components statistics, Table 2. * DBT advises index values should not be relied upon for long-term contractual purposes, as they are based on relatively few quotes.

On a monthly basis, the greatest price increase was a 5.5% rise in prices for bituminous mixtures based on natural and artificial stone. The steepest decrease was a 0.5% fall in cement prices.

The latest Builders Merchant Building Index (BMBI) report(3), which analyses market trends using data from the Builders Merchant Panel produced by GfK (Growth from Knowledge), a subsidiary of NielsenIQ (NiQ), shows that builders merchants like-for-like volume sales in April 2026 were 3.5% lower than in April 2025.

Like-for-like value sales also decreased by 0.6% in this period while average prices were up by 3.0%.

The report suggests that the Renewables and Water category recorded the greatest annual price increase, up by 17.5%, likely connected to the 20.5% fall in volume sales between April 2025 and April 2026.

‘As expected, the latest BMBI insights suggest that builders merchants are increasing prices in response to weaker demand and lower sales volumes,’ Dr Crosthwaite said. ‘This trend is evident across several product categories, including Renewables and Water, Tools, Heavy Building Materials and Landscaping.

‘The root cause is weaker demand across the construction sector. However, with tensions in the Middle East appearing to ease, there is hope that construction activity will begin to recover. As demand for construction increases, demand for certain products should also strengthen, helping to normalise supply chains and ease inflationary pressures on contractors’ input costs. That said, it will likely take a few months for these effects to filter through and for the market to rebalance.’

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.