BCIS CapX provides a comprehensive, detailed and easy-to-use method of measuring cost movement for building and civil engineering. Widely used in the construction and infrastructure sector to help fairly allocate risk between the client and sub-contractors.

Published: 10/04/2026

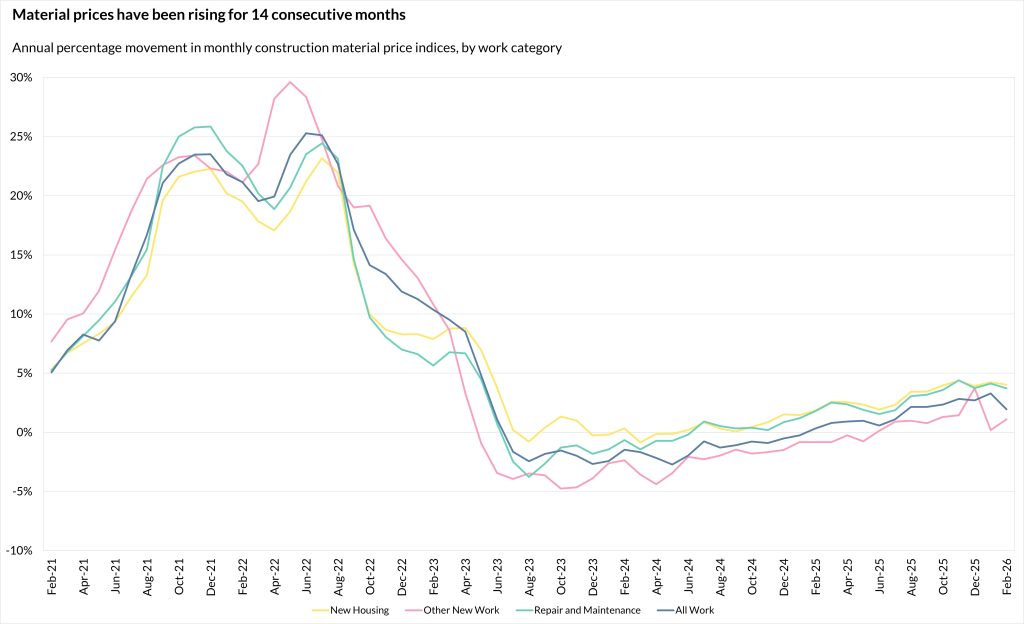

Each month the Department for Business and Trade (DBT) publishes construction material price indices (CMPIs), categorised under All Work, New Housing, Other New Work and Repair and Maintenance, as well as tracking a selection of building materials and components for the UK(1). BCIS data is used in the compilation of the DBT indices(2).

Construction material prices see sustained growth in February

Construction material prices for All Work rose by 2.1% in the 12 months to February 2026, according to the latest provisional data published by DBT.

New Housing recorded a 3.4% increase, Other New Work rose by 1.1%, and Repair and Maintenance increased by 2.7% when comparing February 2026 with February 2025.

DBT’s CMPIs are compiled using a combination of resource cost indices produced and published by BCIS. These are based on BCIS Price Adjustment Formulae Indices (PAFI).

Source: Department for Business and Trade – Building materials and components statistics, Table 1a

Dr David Crosthwaite, chief economist at BCIS, said: ‘Materials prices remain elevated and in light of recent anecdotal evidence, prices may have already shifted to a higher base as inflationary pressures linked to Middle East tensions take effect. Next month’s data should hopefully provide a clearer picture.

‘At present, ceasefire negotiations, the success of which remain tentative, and the prospect of near-term conflict resolution represent the best-case scenario for construction. However, even under these conditions, shipping routes will take time to normalise, as will the recovery of damaged or destroyed energy infrastructure. Both factors are likely to sustain elevated materials costs and by extension tender prices, with movement in both also dependant on demand.’

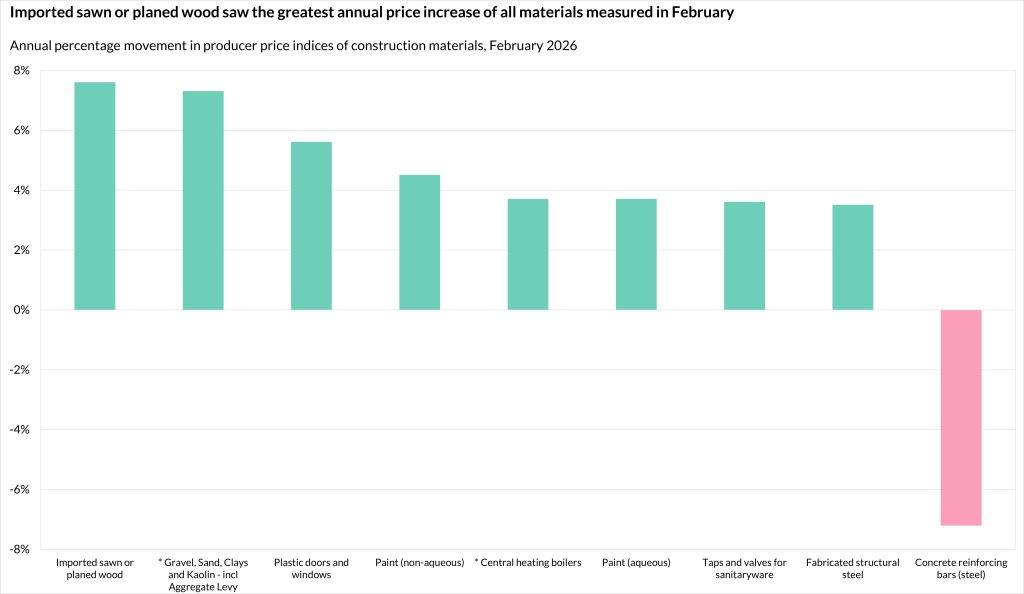

DBT data also show that prices for imported sawn or planed wood saw the greatest inflation in the 12 months to February 2026, up by 7.6%. This was followed by a 7.3% rise in prices for gravel, sand, clays and kaolin (including the Aggregate Levy).

Prices for concrete reinforcing bars (steel) again saw the steepest annual decrease of all resources measured with a 7.2% fall.

Source: Department for Business and Trade – Building materials and components statistics, Table 2. * DBT advises index values should not be relied upon for long-term contractual purposes, as they are based on relatively few quotes.

On the month, fabricated structural steel experienced the greatest price increase with a 2.7% rise.

The steepest decrease was a 1.8% fall in prices for gravel, sand, clays and kaolin (excluding the Aggregate Levy).

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.