The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance.

Published: 14/07/2026

Geopolitical tensions are feeding into construction tender prices, but the picture is more nuanced than it first appears

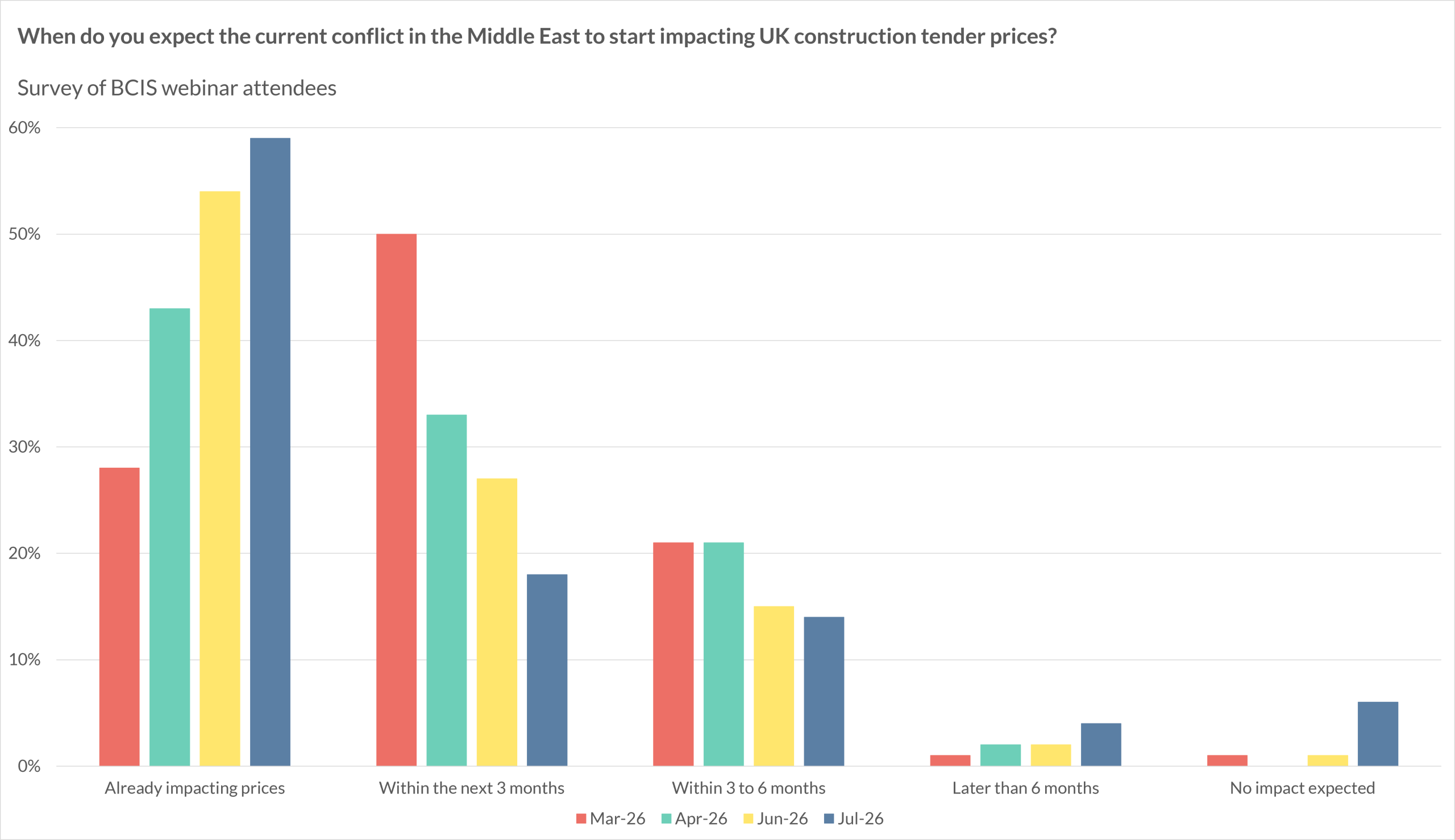

When BCIS polled construction professionals in March 2026, less than a month after the US’s first air strikes on Iran, just over one-quarter said the conflict in the Middle East was already affecting UK construction tender prices. By July, that figure had risen to 59%. Taken at face value, the trend points to a market increasingly feeling the effects of geopolitical disruption. The reality, however, is more complicated.

The shift in sentiment is striking and should not be dismissed. Each month, the proportion of professionals (the majority cost consultants and surveyors) reporting an impact has grown, while the share expecting to see one in the future has fallen as those expectations have seemingly been realised. In March, half of those polled anticipated an impact within three months. By July, that figure had dropped to 18%.

Source: BCIS

Note: Responses given anonymously, sample sizes range from 250 to 396.

Yet when the BCIS TPI panel, made up of cost consultants from firms involved in multiple tenders each quarter, met in June, members reported that the conflict in Iran had not yet fed through into tender prices in any significant or widespread way. Crucially, the panel noted that low activity levels continue to offset inflationary pressures on input costs, and that any price increases arising from recent geopolitical developments were expected to materialise later rather than immediately. The BCIS All-in Tender Price Index increased by 1.0% between 1Q2026 and 2Q2026, resulting in annual growth of 3.2% from 2Q2025.

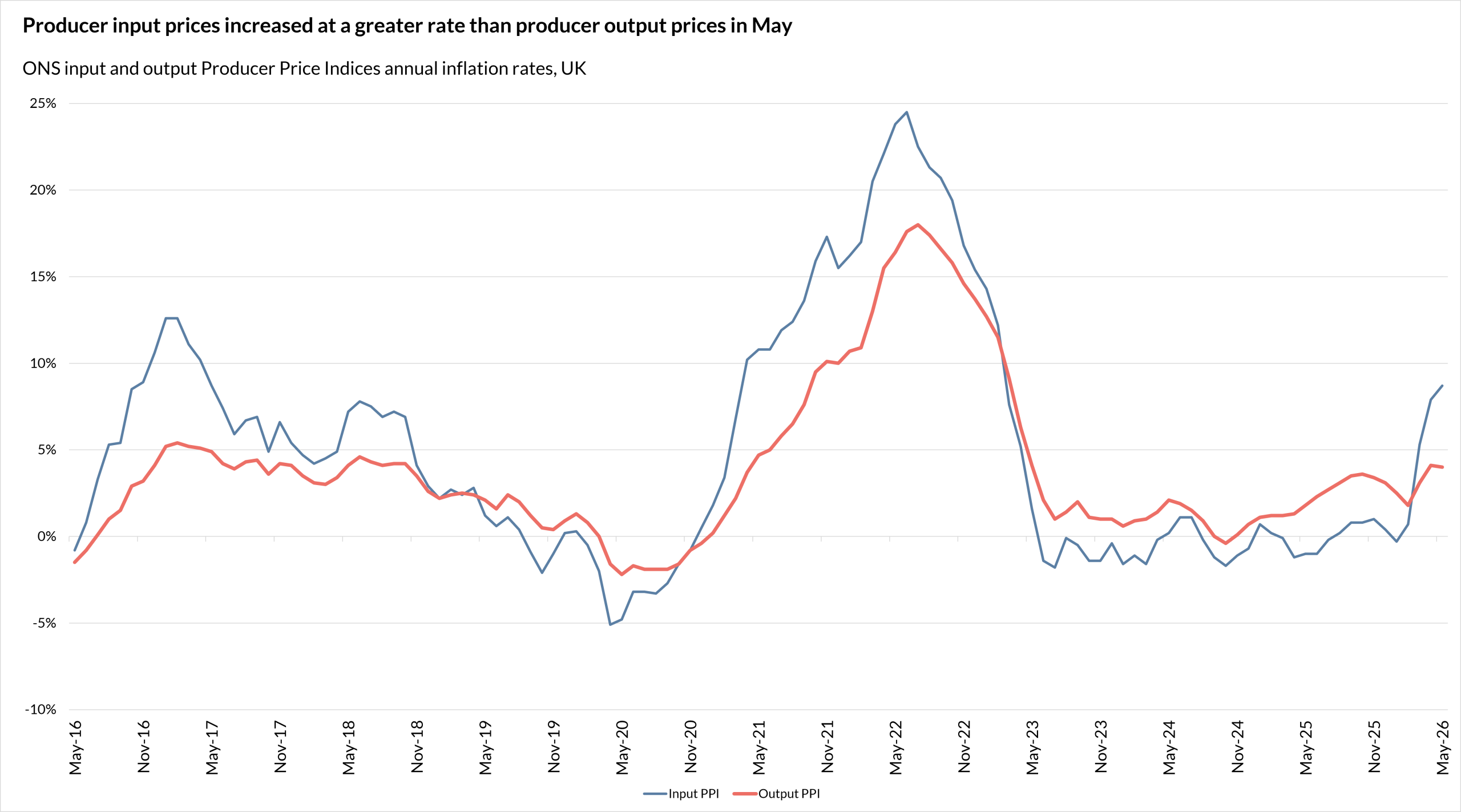

Reconciling these two pictures requires looking at what is happening at different points in the supply chain. The BCIS TPI panel reported evidence of cost increases across a range of energy-intensive materials, including steel, glass, cement, bricks, aluminium, insulation and pre-cast concrete. The ONS producer price data for May 2026 reinforces this picture: producer input prices rose by 8.7% in the year to May, the largest annual increase since February 2023, driven primarily by crude oil, which rose by 71.8% over the same period. Yet producer output prices rose by just 4.0% annually, a gap of more than four percentage points, with basic metals, fabricated metal products and machinery up 4.2% year-on-year. The divergence between what manufacturers are paying and what they are charging is itself evidence of margin absorption rather than cost pass-through, and it mirrors the dynamic the BCIS TPI panel is observing further up the supply chain at the tender price level.

Source: ONS

Timing is also a factor. The gap between input cost movements and their appearance in tender prices is well-established, and the lagged nature of construction cost data means that early market movements can take months to feed through to headline figures. The input PPI rose by just 0.2% in May on a monthly basis, following a more significant 2.6% rise in April, suggesting some stabilisation, though annual pressures remain acute. The full effects of the current geopolitical environment are still working their way through supply chains.

Weak demand is providing a further dampening effect. With construction activity having contracted for 18 consecutive months, according to the latest S&P Global UK Construction Purchasing Managers’ Index, contractors continue to operate in a competitive market. Two-thirds of respondents to the BCIS TPI panel survey identified contractors as eager to tender in the second quarter, with competition intensifying as the flow of new work slows. That competitive pressure limits the extent to which rising input costs can be passed on to clients, even where those cost pressures are genuine. The panel drew a direct comparison with the Ukraine conflict, noting that demand conditions are considerably weaker now than they were during the early stages of that episode, leading to expectations that price increases may not reach the same peaks experienced previously.

The pricing environment is therefore more differentiated than any single headline figure might suggest. Some projects, particularly those involving energy-intensive materials or long procurement programmes, are already seeing cost pressures reflected in the prices being returned. Others, in more competitive segments of the market, may see those pressures emerge more slowly. The panel also cautioned that contractor margins have been squeezed to the point where cost increases can no longer be absorbed in all cases, raising the prospect of supply chain stress and an increase in insolvencies if conditions persist.

Applying a uniform inflation assumption across a project, or relying solely on headline index movements, is unlikely to capture the full picture in the current environment. Understanding which elements of a project are most exposed to geopolitical cost pressures, and how contractor pricing behaviour is likely to respond as demand recovers, is increasingly important for producing cost plans that are robust enough to withstand a rapidly evolving market.

BCIS subscribers can access the full tender price forecast, alongside the latest input cost indices and TPI panel commentary, via BCIS CapX.

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.