The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance.

Published: 01/08/2025

Wage awards published in the last couple of months point to a sector adjusting to calmer inflation levels, but widely reported skills shortages could put pressure on pay when activity picks up. Dr David Crosthwaite, chief economist at BCIS, assesses what we can learn from the latest agreements.

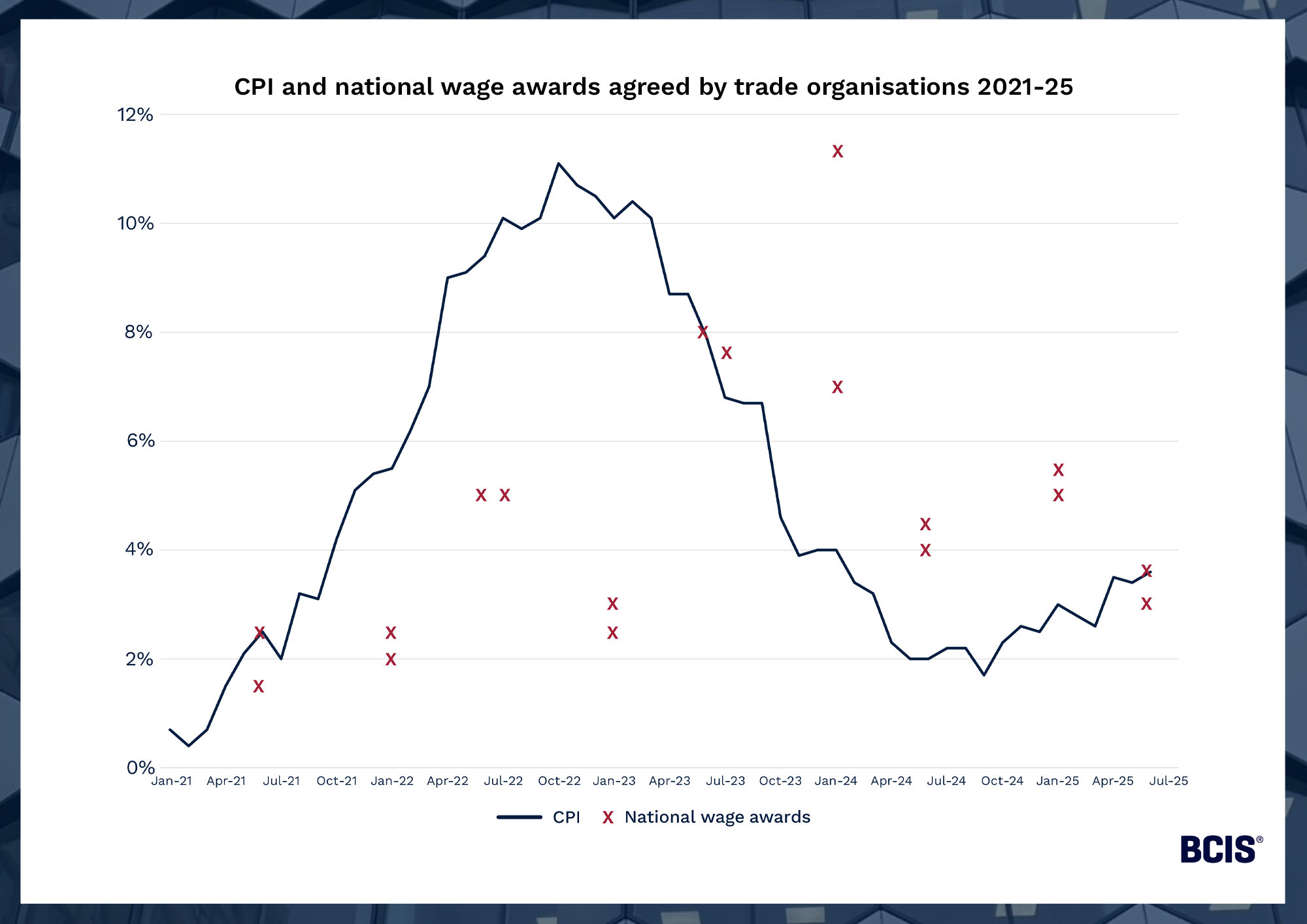

After a run of steep increases, wage awards in construction appear to be settling down. This summer, national agreements by the Construction Industry Joint Council (CIJC) and Building and Allied Trades Joint Industrial Council (BATJIC) have seen uplifts of 3.2% and 3.6% respectively, applicable from June 2025. These are notably lower than the pay increases of 5-8% agreed by some trades in 2023 and early 2024, and especially the 11.3% awarded to steelworkers in January 2024.

Source: ONS, BATJIC, CIJC, JIB, JIB-PMES, NJC

Wage awards tend to follow the broader inflation trend, albeit with a lag, as employers and trade unions negotiate based on inflationary pressure in the recent past. When CPI peaked at 11.1% in October 2022, wage awards remained comparatively subdued in the immediate aftermath. As CPI dropped through 2023–24, settlements rose to catch up, reflecting the delayed response built into annual review cycles.

Now, with CPI hovering around 3.5% and forecasts pointing to stabilisation near the Bank of England’s 2% target over the next couple of years – further economic shocks excepting – recent wage settlements show signs of moderation and, in the case of the CIJC and BATJIC June awards, are in line with the current CPI rate. This marks a shift from recent years, when pay awards often exceeded inflation to recover real-terms losses experienced during the 2022 inflation spike.

This softening likely reflects wider economic pressures. Rising employment costs, such as the increase to employers’ National Insurance Contributions effective from April 2025, are encouraging firms to manage pay growth more cautiously. At the same time, vacancy levels are falling and unemployment has ticked up, reducing the upward pressure on wages that has dominated recent years.

However, the labour market picture remains complex. Structural shortages in certain construction trades persist, and while wage growth may have moderated for now, the underlying supply constraints haven’t gone away. Employers may still need to compete for key skills, especially when demand rebounds.

It’s also worth noting that, as materials cost inflation has eased significantly from the 2021-2022 peaks, labour costs have become the more prominent driver of project cost growth. The BCIS Labour Cost Index showed an annual rise of 7.3% in June 2025, while the BCIS Materials Cost Index increased by just 0.2% over the same period. With materials inflation relatively stable, pay rates are playing a greater role in shaping tenders and long-term cost plans.

Although current wage awards suggest the industry has moved beyond the double-digit pay rises seen in recent years, it’s too soon to assume labour costs will remain flat. Wage outcomes reflect both inflation and market demand, and if construction activity picks up, particularly under a government focused on infrastructure and housing delivery, that could bring renewed upward pressure on pay.

While there are signs of stabilisation, future wage settlements will continue to reflect broader economic conditions. Barring further shocks, labour costs may not spiral, but they’re unlikely to stand still.

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.

Share on social media

![]()