The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance.

Published: 27/04/2026

Analysis of housing supply indicators suggests that housing delivery in England saw a modest uptick in the first quarter of the year.

Energy Performance Certificate (EPC) lodgement data for new dwellings, published by the Ministry of Housing, Communities and Local Government(1), indicate that around 48,000 net additional homes were delivered in 1Q2026, a 6% increase on the same quarter in 2025.

In the 12 months to March 2026, around 204,000 EPCs were lodged for new dwellings, a 2% increase on the previous year.

In the context of this data, new dwellings also includes conversions and changes of use. Since EPC lodgements are published more frequently than the annual net additional dwellings statistics, they can provide a more timely indication of housing delivery within the year, and how closely aligned delivery is with the government’s 1.5 million new homes target.

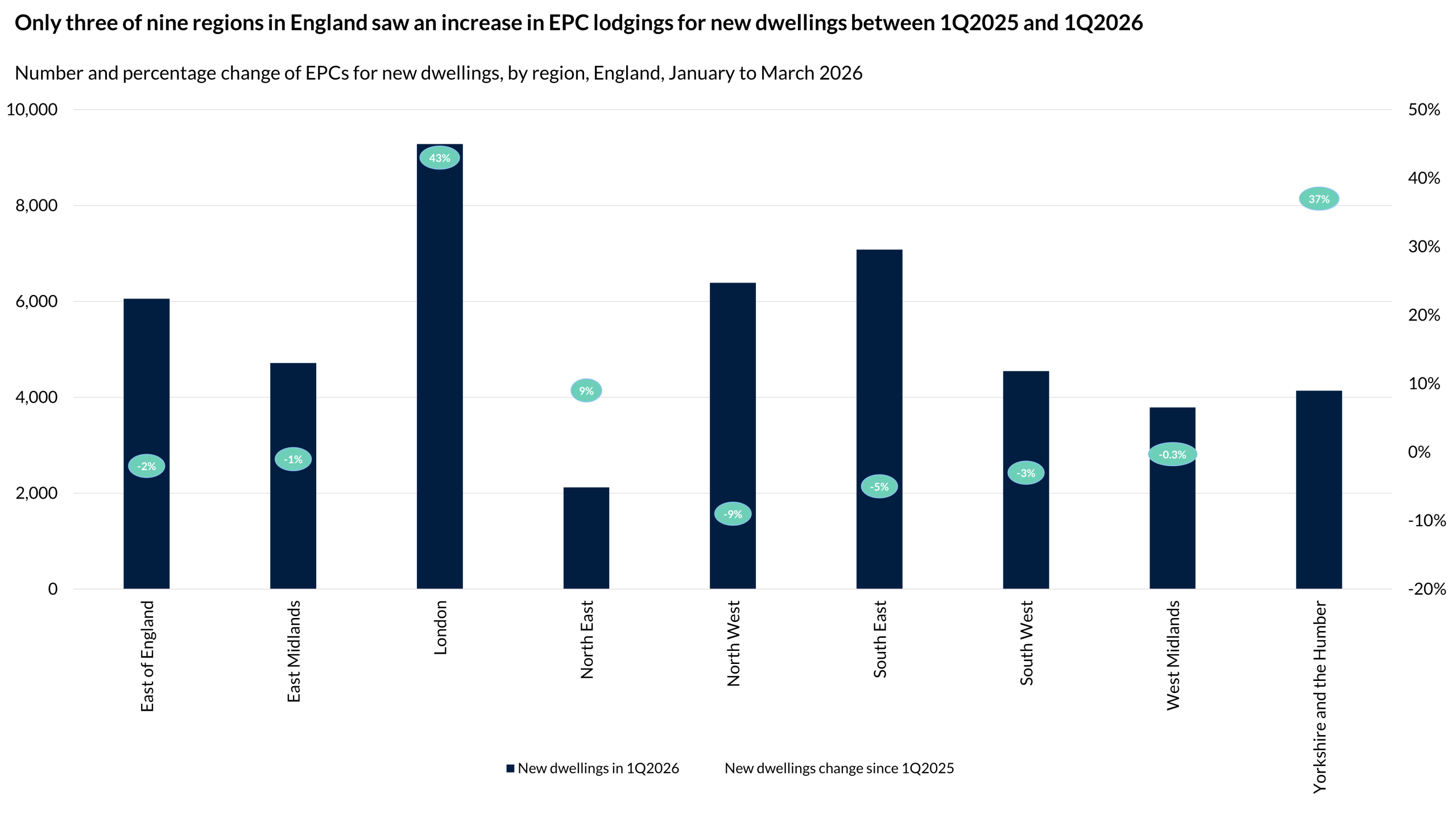

On a regional basis, the greatest increase in EPCs lodged for new dwellings between 1Q2025 and 1Q2026 was in London (43%), while the largest decrease was in the North West (-9%).

Recent trading updates from major housebuilders suggest that a modest improvement in delivery reflects a market that had been stabilising. Barratt Redrow reported a solid update(2) for its trading quarter up to 29 March 2026, with resilient demand and strong forward sales, indicating stable near-term activity.

However, the company also noted that geopolitical developments in the Middle East are contributing to increased economic uncertainty, including the potential for higher energy costs, renewed build cost pressures and a more prolonged, higher interest rate environment. These factors are expected to feed through into the construction supply chain over the coming months.

In addition to global factors, domestic policy changes will also influence cost pressures. Upcoming regulatory requirements, including the Future Homes Standard, alongside measures such as the Building Safety Levy and potential changes to landfill tax, are expected to increase the cost of delivery. While the timing and scale of impact will vary, these factors are likely to place additional pressure on housebuilders, particularly where margins are already constrained.

Taken together, this suggests that while housing delivery has shown some short-term improvement, the outlook remains sensitive to cost pressures and wider economic conditions.

Dr David Crosthwaite, chief economist at BCIS, said: ‘EPC data provide a useful indicator of housing delivery, particularly given the lag in official net additional dwellings statistics. The increase in the first quarter compared with last year is encouraging, but it needs to be viewed in the context of the current backdrop to the sector.

‘The market is not yet showing sustained, broad-based recovery, and we have the cost implications of conflict in the Middle East beginning to feed through. This wider economic uncertainty, as well as regional variations in progress, suggest that delivery could remain uneven over the course of the year.

‘In addition to the potential uplift in costs stemming from higher energy and manufacturing inputs, the current climate of uncertainty is also likely to weigh on homebuyer confidence, which could influence demand and, in turn, the pace of delivery over the coming months.’

Source: Live tables on Energy Performance of Buildings Certificates

To keep up to date with the latest industry news and insights from BCIS register for our newsletter here.